How Do Business Loan Brokers Get Paid?

Brokers earn 1–15% of the funded amount, paid by the lender at funding. Lower on SBA and term loans, higher on short-term advances. Reputable brokers never charge the borrower upfront.

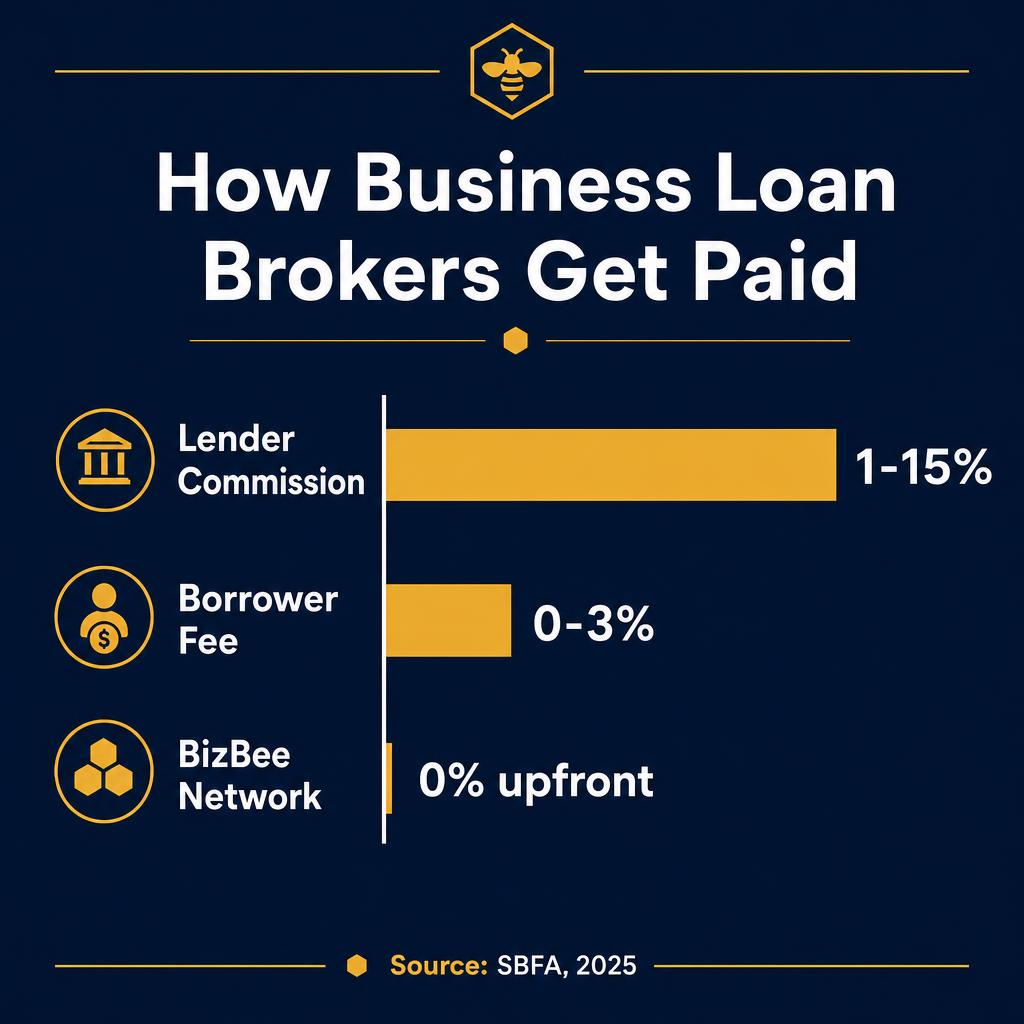

Business loan brokers earn a commission paid directly by the lender when a deal funds, typically 1–15% of the funded amount depending on product (low for SBA/term loans, higher for short-term advances). Reputable brokers like BizBee charge zero upfront fees to the borrower; the commission comes out of the lender's existing margin, not added on top of the borrower's rate.

Key takeaways

- Commission is paid by the lender, not the borrower.

- Typical commission: 1–3% (SBA, term loans), 4–8% (LOC), 6–15% (MCA, short-term).

- Commission comes from the lender's margin, not added to your rate.

- Upfront 'application' or 'processing' fees from a broker are a red flag.

- Per SBFA standards, brokers must disclose how they're paid on request.

- Some niche brokers also charge a borrower-side success fee (0–3%) — must be disclosed in writing upfront.

Who this is for

Owners who want to know exactly how their broker makes money before signing anything.

Anyone comparing broker vs. direct and trying to understand the true cost structure.

What you need to qualify

Typical commission ranges by product type (paid by the lender).

| Requirement | Typical standard |

|---|---|

| SBA 7(a) / 504 | 0.5%–2% of funded amount |

| Bank term loan | 1%–3% |

| Online term loan | 2%–5% |

| Business line of credit | 3%–8% |

| Equipment financing | 2%–5% |

| Merchant cash advance / short-term | 6%–15% |

How broker commissions actually work in business lending

When a deal funds through a broker, the lender wires the borrower the loan proceeds and separately wires the broker a commission. The commission is calculated as a percentage of the funded amount, typically between 1% and 15% depending on the product. It comes out of the lender's existing margin, the same spread that already prices the loan, so the borrower's rate is identical whether they came in direct or through the broker.

The structure exists because lenders prefer paying a commission to qualified, pre-screened files rather than spending the same money on their own marketing and underwriting. A good broker pre-qualifies the borrower, packages the documents, and answers underwriting questions — reducing the lender's cost per funded deal even after the commission is paid.

Why MCA broker commissions are higher than SBA

An SBA 7(a) loan might pay a broker 0.5%–2% of the funded amount because the lender's own margin on a 10.5%–14% SBA loan is thin. A 6-month merchant cash advance might pay a broker 6%–15% because the lender's effective margin on a 1.30 factor rate (60–80%+ APR equivalent) is significantly larger. The commission is sized to the lender's economics, not to a target borrower cost.

Crucially, the borrower's price is the same either way. The factor rate on a 1.30 MCA is 1.30 whether you got it through a broker or directly from the funder. Broker commissions do not raise the price, they shift where the lender's margin gets spent.

Yield spread premium and the one practice to avoid

Yield spread premium (YSP) is the one practice that does cost the borrower. It happens when a broker accepts a higher commission for placing a borrower at a higher rate than they qualified for. Reputable brokers, and SBFA member firms, do not accept YSP. The way to confirm is simple: ask in writing for the lender's underlying quote sheet alongside your final offer. The numbers should match.

If a broker refuses to share the underlying quote, or if the final rate is materially higher than what your file would have qualified for direct, walk away. Lender-paid commission is fine; lender-paid commission funded by a padded borrower rate is not.

What 'no upfront fee' really means, and what to verify

A reputable broker should not charge any of the following before funding: application fee, processing fee, document preparation fee, underwriting fee, packaging fee, or 'good-faith deposit.' Each of these is a hallmark of advance-fee fraud — the broker takes the money, then claims the file was declined and disappears. The FTC has pursued enforcement actions against advance-fee broker schemes for over a decade.

Verify by asking three direct questions in writing: (1) Are there any fees of any kind I will be asked to pay before funding? (2) Will you provide an engagement letter that names every borrower-side fee, including any success fee, before underwriting? (3) Can I see your standard fee schedule? An honest broker answers all three in plain language; a predatory one stalls or pivots to urgency.

How SBA broker compensation is regulated differently

SBA-loan brokers (referred to as 'agents' under SBA rules) must complete SBA Form 159 disclosing the compensation paid by either the lender or borrower for SBA 7(a) and 504 transactions. SBA caps and audits these fees: anything above 1% of the loan amount on loans under $1M, or above $30,000 in absolute terms on loans over $1M, requires additional documentation and justification of services rendered.

This regulated regime is why SBA broker commissions are notably smaller than short-term advance commissions. The trade-off for the broker is that SBA loans are larger in absolute dollar terms, 1.5% of a $750K SBA loan is still $11,250, and SBA borrowers tend to be long-term referral sources. Reputable BizBee partners specifically segment SBA work from short-term work because the deal economics, compliance posture, and closing timelines look almost nothing alike.

How to decide if this is right for you

Three questions confirm a broker's compensation is structured honestly.

-

1

Is the broker willing to disclose how they're paid in writing?

Reputable brokers will explain commission structure, range, and source on request. Refusal or evasion is a hard disqualifier.

-

2

Is there any borrower-side fee — upfront or success?

Upfront fees are predatory and disqualifying. A small disclosed success fee (0–3%) is legal but must be in writing before underwriting begins.

-

3

Will the broker provide the lender's underlying quote sheet?

Yes confirms no YSP. No or stalling suggests the borrower's rate may be padded to fund a larger commission.

When this makes sense

- You want full transparency on how your broker makes money before submitting docs.

- You're comparing offers and want to confirm no hidden borrower-side fee.

When to be careful

- Broker can't or won't explain their commission structure.

- Broker charges any upfront fee.

- Broker adds a borrower-side 'success fee' without disclosing it before underwriting.

How this plays out in practice

SBA 7(a) borrower comparing direct and broker

Situation: Established business taking out a $500K SBA 7(a) loan; deciding between Live Oak direct and a broker.

Recommendation: Either path is fine. SBA commissions are small (0.5–2%) and the lender's price is the same. Pick based on advisor support and turnaround speed.

Restaurant taking a $50K MCA through a broker

Situation: Restaurant accepting a 1.32 factor advance over 9 months; broker is earning ~8% commission.

Recommendation: The 8% commission is normal for MCA. The borrower's cost is 1.32 either way. Confirm the factor matches the lender's underlying quote sheet to rule out YSP.

Broker quoting a 'success fee' on top of lender commission

Situation: Broker discloses a 2% borrower-side success fee in addition to lender-paid commission.

Recommendation: Legal if disclosed in writing pre-underwriting. Compare the all-in cost against another broker that charges no borrower-side fee, usually cheaper.

Broker asking for a $1,500 'document preparation' fee upfront

Situation: Owner is told the fee secures the file's place in underwriting and is refundable if declined.

Recommendation: Walk away. Upfront fees of any kind violate SBFA standards and are the single most common hallmark of advance-fee fraud. Refund promises are routinely broken.

100% transparent fee model

BizBee charges zero upfront fees and is paid only when your deal funds, entirely by the lender.

Frequently asked

Common questions

Key facts in one line

- Business loan broker commissions typically run 1–15% of the funded amount, paid by the lender, not the borrower.

- Reputable brokers never charge upfront fees per Small Business Finance Association (SBFA) standards.

Glossary

Terms worth knowing

- Funded amount

- The dollar amount actually wired to the borrower at closing, the basis on which broker commissions are calculated.

- Yield spread premium (YSP)

- Extra commission a lender pays for placing a borrower at a higher rate than they qualified for. Reputable brokers refuse YSP.

- Success fee

- A small (0–3%) borrower-side fee some brokers charge on funded deals. Must be disclosed in writing before underwriting.

- Origination fee

- A lender-charged fee (typically 1–5% of funded amount) netted from the loan proceeds at closing. Not a broker fee.

- SBA Form 159

- Required SBA disclosure form listing all fees paid to brokers, agents, or packagers in connection with an SBA 7(a) or 504 loan. Both borrower and agent sign.

- Advance-fee fraud

- A scheme in which a broker collects fees upfront, application, processing, document prep, then fails to deliver funding. Prohibited under SBFA standards and FTC-actionable.

Ready to Join the Hive?

Apply now via BeeLine™ and get your funding decision in minutes. Complete in less than 60 seconds.