How Does a Merchant Cash Advance Work?

Funder pays you a discounted lump sum today, then auto-debits a fixed daily or weekly amount from your bank account until the agreed total revenue is delivered. No interest, no fixed term — duration depends on debit speed.

An MCA funder buys an agreed dollar amount of your future business revenue (the "purchased amount") at a discount (the "purchase price"). You receive the purchase price as a lump sum, then deliver the purchased amount by sending a fixed daily or weekly ACH from your business checking until the total is satisfied.

Key takeaways

- Three numbers define every MCA: advance amount, factor rate, and total payback.

- Daily or weekly ACH is fixed at funding, it does not float with your revenue (unlike legacy split-funded MCAs).

- Estimated term = total payback ÷ daily payment × business days per month.

- If revenue drops, you can request a reduction ("reconciliation"), but it's not automatic and not guaranteed.

- Stacking a second MCA on top of an active one usually breaches the first contract.

Who this is for

Owners considering an MCA who want the mechanics in plain English first.

Businesses already in an MCA who want to understand reconciliation, payoff, and renewal options.

What you need to qualify

| Requirement | Typical standard |

|---|---|

| Time in business | 4+ months |

| Monthly revenue | $10,000+ |

| Bank statements | Most recent 4 months |

| Credit | 500+ FICO (often) |

The contract math

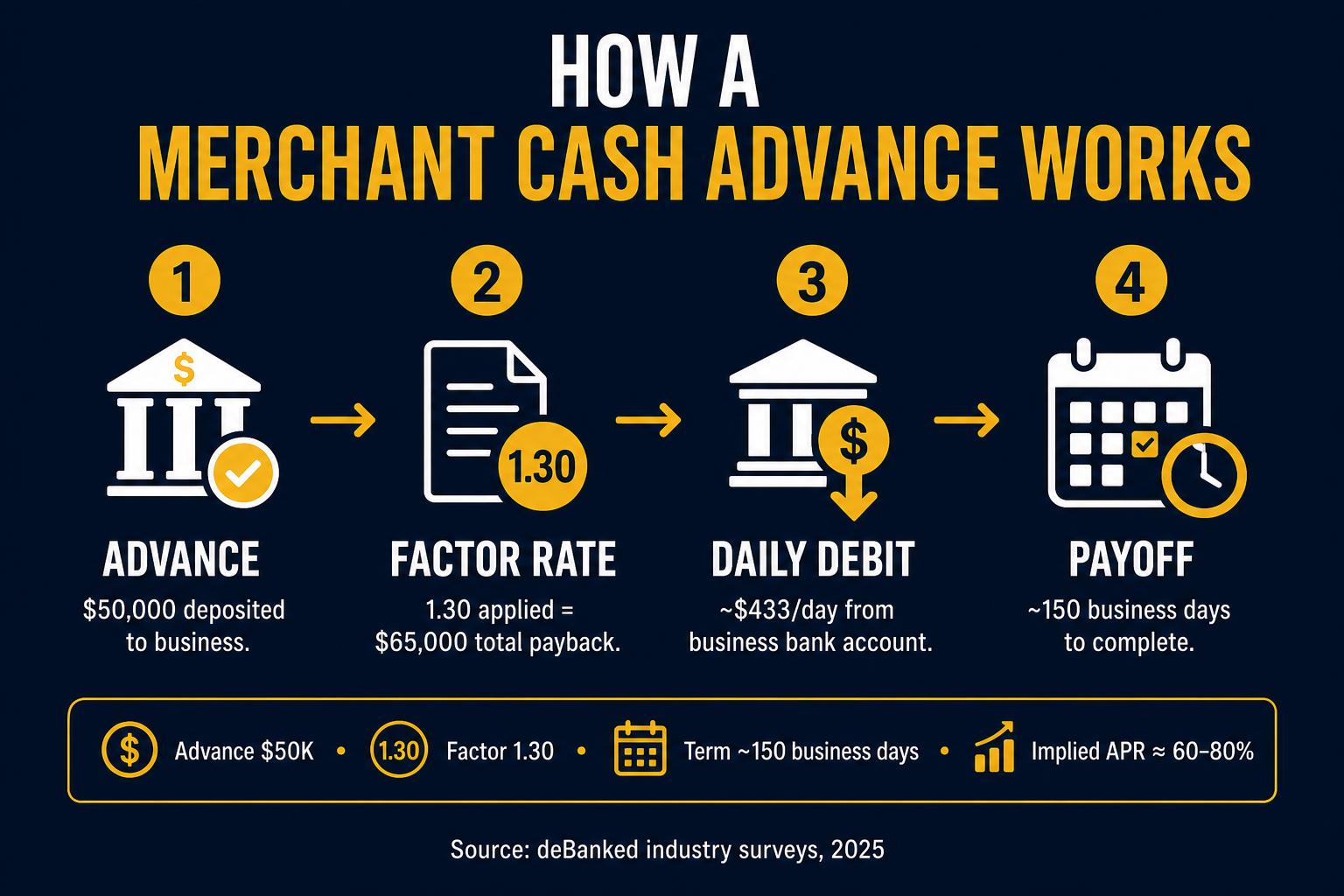

Funder advances $50,000 at a 1.30 factor. Total purchased amount: $65,000. Fixed daily ACH: $295 over ~10 months. There is no interest accruing, the $15,000 spread is the entire cost, locked at funding.

Daily ACH holdback

Modern MCAs debit a fixed dollar amount, not a true % of revenue. Plan worst-week cash flow around the fixed daily debit, not your good weeks. If revenue falls, you may qualify for reconciliation — read the contract clause.

Reconciliation

If actual revenue drops materially, you can submit recent bank statements and request the daily debit be temporarily lowered. Reconciliation is contractual but funder-discretionary. Document everything.

Renewal and stacking

Around 50%–70% paid down, the funder may offer a renewal (net new capital + payoff of remainder). Stacking with another MCA, without payoff, almost always breaches the original contract and damages future approvals.

How factor rate, payback term, and effective APR fit together

The factor rate (typically 1.18–1.45 in 2026) is the multiplier, advance $50K at factor 1.30 and the purchased amount is $65K. The cost spread ($15K) is locked at funding regardless of how long repayment takes. Repayment speed is what converts that flat cost into an annualized rate, and a faster payback dramatically raises the effective APR. The simple-formula conversion of (factor − 1) × (365 ÷ days to repay) understates true APR by 30%–80% on daily-debit products because the average outstanding balance falls quickly across the term.

Worked example: $50K at factor 1.30, $295/day debit, 220 business days to repay (roughly 10 months). Simple-formula APR = 0.30 × (365 ÷ 300 calendar days) = 36.5%. Effective APR with daily amortization: roughly 60%–75%. This is why an MCA quoted as 'about 30%' usually carries a true APR in the 50%–80% range. Any honest MCA comparison needs the effective APR, not the factor rate or the simple-formula conversion.

Three practical implications. First, slower payback at the same factor is always cheaper in APR terms (and in monthly cash-flow burden) than faster payback. Second, prepaying an MCA generally does not reduce total cost because the purchased amount is fixed, early payoff savings happen only on the rare 'early discount' clause. Third, when two factor offers have identical total dollars, choose the longer term every time.

What underwriters actually score on a 2026 MCA application

Modern MCA underwriting is built around four months of business bank statements, with five line items weighted heavily: average daily balance (target $3K+), monthly deposit count (10+ is strong, fewer than 5 raises flags), NSF count (zero in 90 days unlocks the best tiers; 3+ usually triggers decline), negative-day count, and presence of existing MCA debits (a single active MCA is acceptable to many funders, two is a hard stop for most).

Personal FICO matters less than on a term loan — most MCA funders approve at 500+, but FICO still moves pricing. A 500-FICO borrower with $40K/mo deposits typically prices at factor 1.35–1.45; a 650-FICO borrower with the same deposits prices at 1.22–1.30. Industry NAICS, time in business (4+ months is the typical floor), and state of operation also shift pricing by 2–5 factor points depending on the funder.

Documents to expect: the four most recent months of business bank statements (all pages), a one-page application, a driver's license, a voided check, and in some cases a recent tax return for advances above $150K. Funding typically lands in 24–72 hours from a complete file. BizBee pre-qualifies soft-pull before any document submission, so owners can see realistic factor ranges without committing.

Renewal, payoff, and refinance, the back half of the MCA lifecycle

Around 50%–70% paid down, most funders proactively offer a renewal: net new capital plus payoff of the remaining balance, typically at the same or slightly improved factor. Renewals are convenient but rarely cheapest, the new factor is applied to the full new amount (including the old balance being refinanced), so total cost-of-capital effectively double-counts the refinanced portion. Always quote a standalone fresh advance from a different funder before accepting a renewal.

Refinance into cheaper capital is the better long-term play when feasible. Owners who built 6+ months of clean MCA payment history often qualify for working-capital term loans at 22%–35% APR, meaningfully cheaper than the 50%–80% effective APR of the MCA. BizBee advisors model whether a refinance net-saves money before recommending, including any prepayment language in the existing contract. Reverse-consolidation programs (a separate product) can also lower daily debit on multiple active MCAs without triggering a stacking breach.

How to decide if this is right for you

Five checks separate an MCA that works from one that buries the business.

-

1

Model the daily debit against your worst week

Take your lowest 4-week revenue period in the last year. Subtract the daily MCA debit. If that number can't cover payroll + rent, the MCA is too big.

-

2

Confirm the use of funds is ROI-positive in 60–90 days

MCAs are too expensive for slow-payback uses. A new piece of equipment that earns $1,500/day pays for itself; covering a soft month rarely does.

-

3

Read the reconciliation clause word-for-word

Some contracts make reconciliation easy; others make it nearly impossible. Confirm what triggers it, how often you can request it, and what documentation is required.

-

4

Never stack a second MCA on top of an active one

Stacking breaches almost every MCA contract and damages your future approvals at every funder in the network.

-

5

Plan the exit before signing

At 50%–70% paid down, you'll be offered a renewal. Decide in advance whether you'll renew, pay off, or refinance into cheaper capital.

When this makes sense

- You understand the cost, the daily debit, and the use of funds clearly produces more profit than the spread.

When to be careful

- You don't know your average daily revenue net of MCA debit

- You have an active advance and are considering a second

How this plays out in practice

Restaurant funding a clear ROI piece of equipment

Situation: Pizza shop needs a $35K oven that will add $1,200/day in revenue. Has $40K/mo deposits and no other debt.

Recommendation: MCA can work. $35K at factor 1.30 = $45,500 total, ~$170/day for 9 months. Daily payment is fully covered by added oven revenue from day one.

Owner using MCA to cover a soft month

Situation: Retailer takes a $50K MCA to cover three slow months. Revenue doesn't rebound. Owner considers a second MCA.

Recommendation: Stop. Don't stack. Call a BizBee advisor about restructuring before adding more daily debit. Stacking usually accelerates the cash crunch.

Mid-MCA renewal offer at 60% paid

Situation: Owner 60% through a $100K advance, offered a renewal for $75K net new capital + payoff of $40K balance.

Recommendation: Run the math. Renewals often refactor the full balance — true cost of the 'new' $75K can be much higher than a fresh standalone advance. Get a competing quote first.

Talk to a BizBee advisor before signing any MCA

We'll model the daily debit against your real cash flow, free.

Frequently asked

Common questions

Glossary

Terms worth knowing

- Purchased amount

- The total future revenue the funder is buying, the dollar number you'll repay in full (advance × factor).

- Holdback

- The fixed daily or weekly ACH that the funder debits until the purchased amount is delivered.

- Reconciliation

- Contractual mechanism to lower the daily debit if business revenue drops materially. Always funder-discretionary.

- Stacking

- Taking a second MCA while a first is active. Breaches almost every MCA contract and is a major underwriting red flag.

- COJ (Confession of Judgment)

- A clause some funders include allowing them to obtain a court judgment without trial in certain states if you default. Banned in some states; read carefully.

Ready to Join the Hive?

Apply now via BeeLine™ and get your funding decision in minutes. Complete in less than 60 seconds.