Low Credit Business Loans: The Complete Options Menu

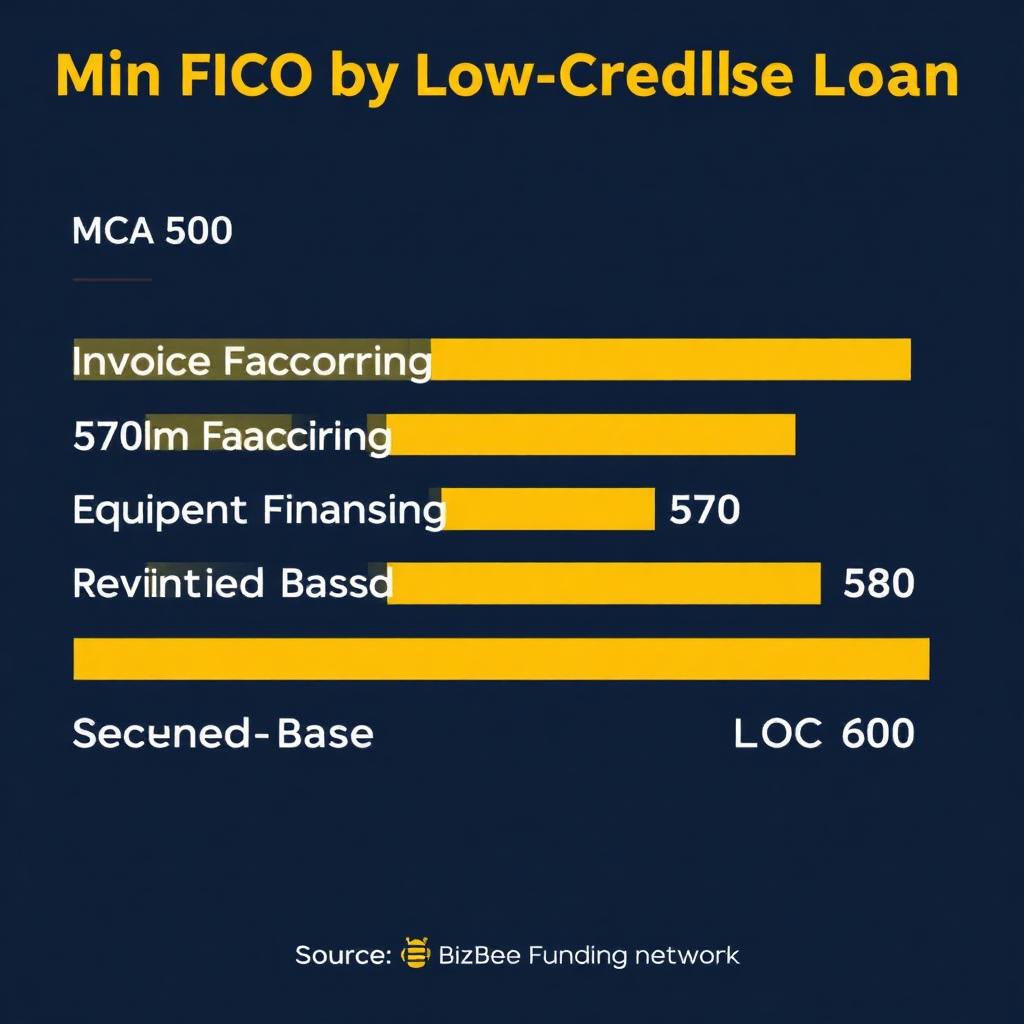

Low-credit business loans (FICO 500–679) come in five legitimate flavors: MCA (FICO 500+), invoice factoring (530+), equipment financing (575+), revenue-based financing (580+), and secured lines of credit (600+). Pricing is higher than prime-credit options, but real funding is accessible. The right product depends on revenue, time in business, collateral, and use of funds.

Low-credit business loans (FICO 500–679) come in five legitimate flavors: MCA (FICO 500+), invoice factoring (530+), equipment financing (575+), revenue-based financing (580+), and secured lines of credit (600+). Pricing is higher than prime-credit options, but real funding is accessible. The right product depends on revenue, time in business, collateral, and use of funds.

Key takeaways

- Five legitimate low-credit business loan products span FICO 500–679.

- MCA starts at FICO 500, fastest funding, highest cost.

- Invoice factoring (FICO 530+) underwrites your customer's credit, not yours.

- Equipment financing (FICO 575+) uses the asset as collateral.

- Revenue-based financing (FICO 580+) flexes payment with revenue.

- Secured lines of credit (FICO 600+) collateralize against AR or inventory.

- Cleanup (NSFs, utilization, collections) can graduate you to prime-tier in 6–12 months.

Who this is for

Small business owners researching low credit business loans who want a clear, advisor-quality overview before making a financing decision.

Operators comparing a current offer against alternative low credit business loans options to confirm they are getting market-competitive terms.

First-time borrowers who want to understand the full low credit business loans landscape before applying.

What you need to qualify

Typical requirements across the BizBee Funding partner network. Specific minimums vary by lender and product.

| Requirement | Typical standard |

|---|---|

| Personal FICO | 500–679 (this guide's bracket) |

| Time in business | 6+ months (12+ for broader options) |

| Monthly revenue | $10,000+ ($25K+ for best low-credit pricing) |

| Bank statements | 3–6 months with ≤3 NSFs |

| Active bankruptcy/unresolved judgment | Disqualifying for most products |

| Existing advances | Disclose upfront — lender will see them |

Best funding options

Product categories available through BizBee's lender network for this topic.

Every Low-Credit Product, Ranked by Accessibility and Cost

Merchant Cash Advance (MCA), Minimum FICO 500. Speed: 24–72 hours. Cost: factor 1.22–1.40, roughly 30–60% APR equivalent. Best for: time-sensitive capital needs at a business with $10K+/mo in card or business deposits. Cautions: daily/weekly ACH debits can strain cash flow on soft weeks; never stack a second MCA before paying off the first.

Invoice Factoring, Minimum FICO 530 (the customer's credit matters more than yours). Speed: same-day to 48 hours after setup. Cost: 1–5% per 30-day period, advance rate 80–95% of invoice. Best for: B2B businesses with creditworthy customers and 30–90 day payment terms. Particularly useful for staffing, trucking, manufacturing, and professional services.

Equipment Financing, Minimum FICO 575. Speed: 1–3 business days with a quote in hand. Cost: 18–30% APR for low-credit tier (vs. 8–18% at 700+ FICO). Best for: revenue-generating equipment with predictable depreciation. The asset serves as collateral, which is why this product approves at lower FICO than unsecured term loans.

Revenue-Based Financing (RBF) — Minimum FICO 580. Speed: 24–72 hours. Cost: factor 1.18–1.45, payment as percentage of monthly revenue (typically 5–15%). Best for: seasonal businesses, businesses with variable revenue, and operators who want payments to flex with sales rather than fixed schedules.

Secured Line of Credit, Minimum FICO 600. Speed: 5–14 days. Cost: 14–28% APR on drawn balance. Best for: established businesses with AR, inventory, or equipment that can be collateralized. The collateral substantially reduces lender risk vs. unsecured LOC.

Products that DON'T realistically approve in the low-credit tier: SBA 7(a) loans (typically 650+ FICO minimum), unsecured bank term loans (680+ typical), prime online term loans (650+ typical), and unsecured LOC (660+ typical). Applying to these with a 580 FICO almost always results in a hard-pull decline that further dings your score.

The best low-credit strategy is to use a tier-appropriate product to fund a high-ROI use of funds, pay it on-time, build operating credit and FICO over 6–12 months, and then refinance into prime-tier products. BizBee Funding routinely helps borrowers cycle from FICO 560 → 640 → 700 by sequencing the right products.

What Lenders Do With a Sub-650 FICO in 2026

A FICO under 650 doesn't disqualify a business from funding in 2026, it shifts which products are realistic and what pricing the file commands. The 2026 lender stack for low-credit files breaks into four tiers: (1) revenue-based financing and MCA (550+ FICO accepted, factor 1.30–1.50, no collateral), (2) equipment financing with the equipment as collateral (580+ FICO, 12–28% APR), (3) invoice factoring keyed to customer credit not yours (500+ FICO, 1.5–4% per 30 days), and (4) secured term loans with real estate or rolling stock collateral (600+ FICO, 12–22% APR).

The single highest-leverage move on a low-credit file is shifting from unsecured to secured. A 580 FICO file applying for unsecured working capital will see factor rates north of 1.45. The same file pledging equipment, real estate, or factoring receivables drops into the 14–24% APR band. The 2026 NerdWallet small-business lending review (May 2026) found secured offers averaged 38% lower total cost than unsecured offers for files in the 550–650 FICO band.

The second-highest leverage move is documented improvement. A 60-day gap between FICO check and submission, used to pay down revolving utilization below 30%, frequently moves a file 20–40 points. That single change can unlock the next pricing tier. Lenders see the soft pull from your advisor's pre-qual; they don't see your subsequent paydown until they pull at submission. Time the paydown 5–7 days before submission so the bureau has updated.

What this typically costs

Representative 2026 cost scenarios. Your actual offer depends on credit, revenue, time in business, and lender.

| MCA (FICO 500–579) | Factor 1.25–1.40 · ≈35–60% APR equivalent |

| Invoice factoring (FICO 530+) | 1–5%/30-day period · advance 80–95% of invoice |

| Equipment financing (FICO 575+) | 18–30% APR · 24–60 month term |

| Revenue-based (FICO 580+) | Factor 1.18–1.45 · 5–15% of monthly revenue |

| Secured LOC (FICO 600+) | 14–28% APR on drawn balance |

| Same products at FICO 700+ | 30–60% cheaper across the board |

How to decide if this is right for you

Use this 5-step framework to narrow your shortlist before comparing specific offers.

-

1

Confirm your actual FICO bracket

Pull current FICO (Experian or MyFICO). Many borrowers are in a higher bracket than they assumed.

-

2

Match product to FICO tier first

Don't apply to products above your tier, hard pulls will damage your file.

-

3

Verify use of funds covers the cost

21% APR on equipment that generates 40% capacity increase = great deal. 21% APR on inventory you can't sell = disaster.

-

4

Clean up before applying if NSFs are present

60–90 days of clean operating history can be the difference between a decline and an approval.

-

5

Plan the graduation path to prime-tier

On-time payments, FICO climb, refinance. 12–18 months is a realistic graduation timeline.

When this makes sense

- Your FICO falls within the tier minimum for the product you need.

- Your monthly revenue and time in business compensate for the FICO score.

- The use of funds clearly generates returns above the all-in product cost.

- You have a 6–12 month plan to graduate to prime-tier financing.

- You've cleaned up NSFs and disclosed any existing advances.

When to be careful

- When you're applying to products above your FICO tier and getting hard-pull declines.

- When you're stacking advances rather than consolidating into one product.

- When the lender doesn't disclose APR or total payback in writing.

- When the contract has a confession-of-judgment clause.

- When you're using low-credit-tier products to fund ongoing operating losses.

How this plays out in practice

The right product for the FICO tier

Situation: Cleaning company with 565 FICO, $28K/mo revenue, 18 months in business. Needed $20K for new equipment.

Recommendation: Equipment financing at 21% APR, 48 months, $608/month. The new equipment increased capacity by 40%, generating $4K/month in incremental revenue. The 'high' rate is irrelevant, unit economics win.

Factoring instead of MCA

Situation: Staffing agency with 540 FICO and $180K in 30-day receivables to Fortune 500 clients.

Recommendation: Routed to invoice factoring at 2.5%/30 days, 88% advance. Got same-day funding without adding debt. Owner's FICO didn't matter because Fortune 500 customers underwrote the deal.

The 12-month graduation story

Situation: Retailer started with 555 FICO and a $30K MCA at 1.42 factor.

Recommendation: Paid on-time, cleaned up personal credit utilization, paid off two collections. FICO climbed to 645 in 11 months. Refinanced remaining MCA balance into a 24-month term loan at 19.5% APR. Total carrying cost dropped 38% over the next year.

580 FICO → equipment-secured term loan

Situation: HVAC contractor with 580 FICO due to medical collections, $35K/mo deposits, needed $60K for a new service van and tools.

Recommendation: Declined twice on unsecured working capital. Restructured as equipment financing with van as collateral: approved at 19.5% APR, 60-month, 10% down. Total cost roughly half the MCA path. Funded day 6.

Find the right low-credit product for your file

Soft-pull prequalification across the five legitimate low-credit product categories. Real offers, real APRs, in plain English. No upfront fees, ever.

Frequently asked

Common questions

Key facts in one line

- Five legitimate low-credit business loan products span the FICO 500–679 range.

- MCA starts at FICO 500; invoice factoring at 530; equipment at 575; revenue-based at 580; secured LOC at 600.

- Same products at FICO 700+ price 30–60% cheaper across the board.

- Low-credit products are best used as a bridge — graduate to prime-tier within 12–24 months.

- Stacking advances is the #1 driver of small-business financial distress in the low-credit tier.

Glossary

Terms worth knowing

- Advance rate

- In factoring, the percentage of invoice value paid to you upfront. Typical: 80–95%.

- Personal guarantee

- A contractual promise that you'll personally repay the loan if the business can't. Standard on virtually all low-credit-tier products.

- Graduation

- The process of refinancing from low-credit-tier products into prime-tier products as FICO and operating history improve.

- Secured vs. unsecured

- Secured loans pledge collateral (equipment, real estate, receivables) and price 30–50% lower than equivalent unsecured offers for low-credit files.

- Revolving utilization

- Personal credit-card balance ÷ limit; paying below 30% within one billing cycle commonly moves FICO 20–40 points.

Ready to Join the Hive?

Apply now via BeeLine™ and get your funding decision in minutes. Complete in less than 60 seconds.