Understanding Small Business Lending: A Comprehensive Overview

Small business lending in 2026 is a multi-channel market: banks, SBA preferred lenders, credit unions, online direct lenders, fintech marketplaces, and brokers. Pricing ranges from ~5% (SBA 504) to ~80%+ effective APR (short-term MCAs). Most small businesses with 6+ months in operation and $10K+ monthly revenue qualify somewhere — the question is which channel and product fit best.

Small business lending is the ecosystem of capital sources, products, and intermediaries that fund U.S. small businesses. The market has six main channels — traditional banks, SBA preferred lenders, credit unions, online direct lenders, fintech marketplaces, and licensed brokers — and ten common products spanning term loans, lines of credit, SBA programs, equipment financing, invoice factoring, working capital, merchant cash advances, revenue-based financing, asset-based lending, and microloans. Per the Federal Reserve's Small Business Lending Survey (Q3 2025), average fixed business loan rates were 6.99%–7.38%, while online and short-term products commonly run 14%–35% APR, and merchant cash advances commonly translate to 60%–80%+ APR per Nav. BizBee Funding operates as a licensed broker connecting small businesses across the channels above to the product and pricing that actually fits.

Key takeaways

- Six lending channels (banks, SBA, credit unions, online direct, marketplaces, brokers) serve the U.S. small business market.

- Ten common product categories cover virtually every legitimate funding need.

- Pricing spans from ~5% (SBA 504) to 80%+ effective APR (short-term MCAs) — channel and product choice matters more than negotiation.

- The Federal Reserve SBLS reports Q3 2025 average fixed rates of 6.99%–7.38% for traditional small business loans.

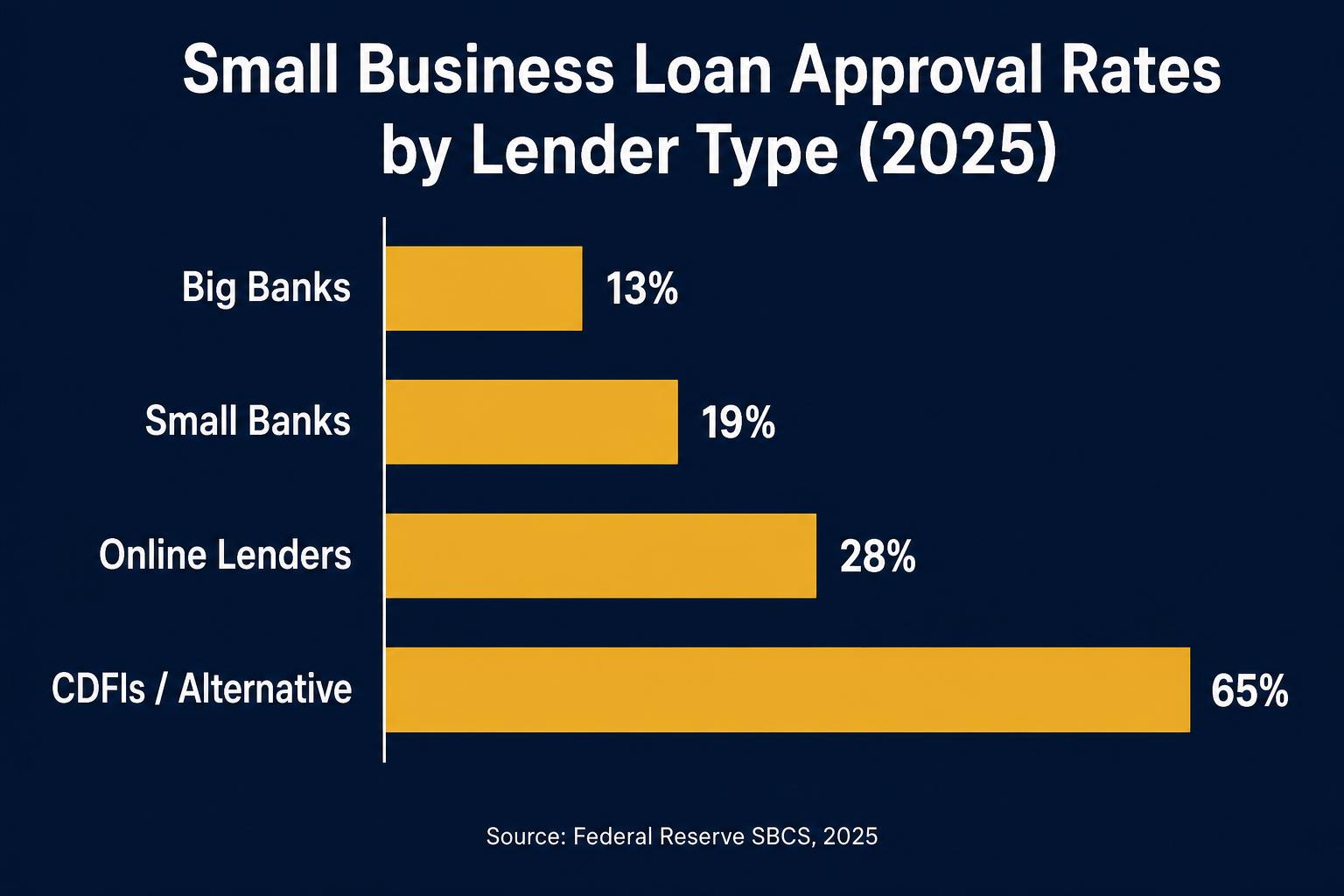

- Banks underwrite tightly and slowly; online lenders underwrite more flexibly and faster — at a price.

- Most established small businesses qualify somewhere — the right question is fit, not feasibility.

- Brokers reduce search cost by pre-vetting lenders and presenting matched offers.

Who this is for

Owners new to small business lending who want to understand the landscape before they apply anywhere.

Operators evaluating whether to refinance existing debt and trying to map the alternatives across channels.

CFOs, controllers, and bookkeepers responsible for setting their company's borrowing strategy and lender relationships.

What you need to qualify

Typical small business lending eligibility across channels. Each channel has its own standards; pulling them together helps you know which doors are realistically open.

| Requirement | Typical standard |

|---|---|

| Bank term loan | 2+ years in business, $250K+ annual revenue, 680+ FICO typical |

| SBA 7(a) / 504 | 2+ years in business, profitable, 680+ FICO, collateral often required |

| Credit union loan | Membership eligibility, similar standards to banks |

| Online term loan | 6–12 months in business, $100K+ annual revenue, 600+ FICO |

| Online line of credit | 12+ months, $150K+ annual revenue, 625+ FICO typical |

| Working capital / MCA | 6+ months, $120K+ annual revenue, 500+ FICO |

| Equipment financing | Often startup-friendly; asset serves as collateral |

| Invoice factoring | B2B with creditworthy customers; lower personal credit OK |

| SBA microloan (≤$50K) | Often newer businesses; community-lender administered |

Best funding options

The six channels that fund U.S. small businesses, with the products each is best at.

Traditional banks

Best pricing on conventional term loans for strong-credit borrowers. Slowest underwriting (2–6 weeks). Tight standards.

SBA preferred lenders

Government-guaranteed loans with the lowest rates available (5%–14.75% range across 504/7(a)/microloan products). 3–6 week timelines.

Credit unions

Member-owned alternatives to banks with similar standards but often better service and slightly more flexibility.

Online direct lenders

Faster underwriting (24 hours to a week) at higher cost than banks. Better access for thinner-credit borrowers.

Fintech marketplaces

Single application distributed to multiple lenders. Convenient but generates high follow-up volume.

Licensed brokers / advisors

Pre-vetted network, single application, side-by-side matched offers. Paid by lenders at closing.

How the Small Business Lending Ecosystem Actually Works

The U.S. small business lending market has expanded dramatically over the past decade as fintech entrants joined traditional banks and SBA preferred lenders. The result is a six-channel market: traditional banks (community, regional, and money-center), SBA preferred lenders (a specific designation granted by the SBA to lenders with proven 7(a)/504 underwriting), credit unions (member-owned cooperatives), online direct lenders (fintech-funded balance-sheet lenders), fintech marketplaces (lead aggregators that distribute applications), and licensed brokers (intermediaries paid at closing).

Each channel serves a different segment. Banks specialize in low-cost conventional term loans for established borrowers with strong credit, collateral, and 2+ years of operating history. The Federal Reserve's Small Business Lending Survey reports Q3 2025 average fixed rates of 6.99%–7.38% on traditional small business loans. SBA preferred lenders specialize in government-guaranteed products: 7(a) loans up to $5 million (capped at $5M per loan, with a cumulative 7(a)+504 limit raised to $10M effective July 4, 2026), 504 loans for real estate and major equipment (5%–7% per NerdWallet, June 2026), and microloans up to $50,000 (8%–13%). Credit unions sit alongside banks with similar standards and often slightly more flexibility for members.

Online direct lenders solved the speed and accessibility problem at the cost of higher pricing. A bank that needs three weeks to approve a $100,000 term loan competes poorly against an online lender that can approve and fund the same amount in 48 hours at 18%–28% APR. For borrowers with 6–12 months in business, $100K+ in annual revenue, and 600+ FICO, online direct lenders unlocked a market the banks could not serve economically. Fintech marketplaces extended this further by collecting one application and distributing it to multiple online lenders simultaneously — but the marketplace model creates lead-volume incentives that often work against the borrower.

Licensed brokers and funding advisors emerged to solve the search-cost problem the marketplace model created. A reputable broker pre-vets its lender network (licensing, complaint history, contract terms, pricing transparency), submits a single soft-pull application to matched partners, and brings the offers back as a curated short list. The broker is paid by the lender at closing, not by the borrower in advance. This is BizBee Funding's model: 100+ vetted lender partners across the bank, SBA, online, and equipment-finance channels; soft-pull-first prequalification; written term sheets and side-by-side comparison before any signature.

Pricing Across the Lending Ecosystem — and Why It Varies So Much

Pricing in small business lending spans a wider range than any consumer credit product. SBA 504 loans price at 5%–7% per NerdWallet (June 2026), bank term loans for strong borrowers at 7%–12%, SBA 7(a) loans at 9.75%–14.75%, online term loans at 14%–35%, business lines of credit anywhere from 3% to 60%+ (Bankrate, with Federal Reserve Q3 2025 averages of 7%–8%), working capital at factor rates of 1.18–1.40 (≈25%–60% APR), and merchant cash advances at factor rates of 1.25–1.50 that commonly translate to 60%–80%+ APR per Nav.

Two things explain this enormous range. First, credit risk: a borrower with 12 months in business and a 580 FICO is statistically far more likely to default than a 5-year business with a 720 FICO, and pricing reflects that. Second, structure and capital cost: a bank lending against its own deposits at the federal funds rate has a much lower cost of capital than a non-bank lender financed by hedge funds at LIBOR+800bps. The bank can price at 9% and still earn a healthy margin. The non-bank lender often cannot price below 18% and remain solvent.

The practical implication: the borrower's job is not to negotiate harder. It is to apply to the right channel. A 5-year, $3M-revenue business with a 700 FICO who applies to an online MCA broker will receive an MCA offer — not because a bank loan would not have been available, but because that was the door they walked through. A reputable broker's value is steering each borrower to the lowest-cost channel they can realistically qualify for, then to the best-priced product within that channel.

What this typically costs

Same $100K loan, six different channels. Total cost over the life of the loan, assuming the borrower qualifies for each (most do not — that is part of the point).

| SBA 504 (real estate) | ~5%–7% APR · ~$10K–$14K interest over 10 yrs (partial) |

| Bank term loan (5 yr) | ~9%–14% APR · ~$24K–$38K total interest |

| SBA 7(a) (10 yr) | ~9.75%–14.75% APR · ~$55K–$85K total interest |

| Online term loan (3 yr) | ~14%–35% APR · ~$25K–$60K total interest |

| Business line of credit | ~7.6%–60% APR on drawn balance (Fed SBLS, Bankrate) |

| MCA (6 mo factor 1.30) | $30K total fee = ~60%–80% effective APR per Nav |

How to decide if this is right for you

Match your profile to the right channel first; product choice comes second.

-

1

Score yourself

Years in business, annual revenue, personal FICO, collateral availability. A 2+ year, $500K+, 700+ FICO profile opens banks and SBA. A 6–12 month, $150K+, 600+ FICO profile opens online direct. Below that, alternative products (MCA, invoice factoring, equipment) become the realistic path.

-

2

Choose the channel before the product

The channel determines the realistic price range. Within a channel, the product choice depends on use case (covered in our 'Types of Small Business Loans' guide).

-

3

Use a soft-pull broker to avoid wasted applications

Each hard credit pull dings your score 5–10 points. A soft-pull broker like BizBee can identify your realistic channel in one application.

-

4

Compare offers in writing

Get the full term sheet — principal, term, payment, fees, total payback, APR — for each offer before signing. Reputable lenders provide this on request.

-

5

Match repayment to revenue

Daily or weekly debits work for businesses with steady daily revenue (retail, restaurants). Monthly payments work for B2B with longer billing cycles. Mismatching the structure creates avoidable cash flow stress.

When this makes sense

- When you understand the channel realistic for your profile before you start applying.

- When you have time to compare at least 2–3 offers in writing.

- When your revenue can support the repayment structure (daily, weekly, monthly).

- When the use of funds has a measurable expected return.

- When you have an advisor or CPA reviewing the contract for non-rate terms (default, prepay, confession of judgment).

When to be careful

- When you apply to a channel that does not match your profile and accept the only offer that comes back.

- When you accept the first offer without comparison.

- When repayment is structured in a way your cash flow cannot reliably absorb.

- When the contract contains a confession of judgment, undisclosed fees, or aggressive prepayment penalties.

- When you are using new debt to service old debt without an underlying operational fix.

How this plays out in practice

Real-world example: the manufacturer who skipped the bank

Situation: A $4M-revenue specialty manufacturer with 12 years in business and a 715 FICO needed $300,000 to expand a production line. He applied to a marketplace and accepted a 24-month online term loan at 22% APR — total interest cost ~$75,000.

Recommendation: He would have qualified for an SBA 7(a) at ~11% over 10 years (~$190,000 total interest, but $1,830/mo vs. ~$15,500/mo) or a bank conventional at ~9.5% over 7 years (~$110,000 interest, ~$4,900/mo). The marketplace cost him about $50,000 in extra interest because he started with the wrong channel.

Real-world example: the new restaurant that started in the right channel

Situation: A 9-month-old restaurant with $35K monthly revenue and a 680 FICO needed $60,000 for kitchen equipment. The owner came to BizBee first.

Recommendation: We placed the equipment financing through a specialized food-service equipment lender at 14% APR over 5 years — total interest ~$22,000. The asset secured the loan, so the rate was meaningfully lower than an unsecured working capital alternative (~28%) and the daily-debit MCA he had been quoted (~62% effective).

Real-world example: the consultant who used a line of credit instead of a term loan

Situation: An independent consultant with $300K annual revenue had a 6-week receivables cycle and occasional 30–60 day cash gaps. He was considering a $50K term loan.

Recommendation: A $75K line of credit at 12.5% on drawn balances replaced the term loan entirely. Average drawn balance: ~$18K for 3 months a year. Annual interest cost: ~$560. A term loan would have accrued interest on the full $50K balance every month. Same operational outcome, much lower cost.

Where does your business fit in the lending ecosystem?

Apply once with a soft credit pull and we'll show you which channel you realistically qualify for — bank, SBA, online direct, or specialized — and present matched offers in writing for side-by-side comparison.

Frequently asked

Common questions

Key facts in one line

- U.S. small business lending operates across six channels: banks, SBA preferred lenders, credit unions, online direct lenders, fintech marketplaces, and licensed brokers.

- Per the Federal Reserve SBLS Q3 2025, average fixed rates on traditional small business loans were 6.99%–7.38%.

- SBA 7(a) loans currently run 9.75%–14.75% per NerdWallet (June 2026), with a $5 million cap per loan.

- Lines of credit can range from 3% to 60%+ APR per Bankrate, with Fed SBLS Q3 2025 averages of 7%–8%.

- Merchant cash advance factor rates of 1.3 on a six-month term commonly translate to 60%–80% effective APR per Nav.

- Most established small businesses qualify for at least three different product categories — the question is which channel and price.

Glossary

Terms worth knowing

- Channel

- The type of institution funding the loan: bank, SBA preferred lender, credit union, online direct lender, marketplace, or broker.

- Preferred Lender Program (PLP)

- SBA designation granting a lender authority to make 7(a) and 504 loans with delegated approval authority.

- Small Business Lending Survey (SBLS)

- Quarterly Federal Reserve publication tracking U.S. commercial bank small business loan volume and rates.

- Underwriting

- The lender's process of evaluating risk before approving a loan.

- Cost of capital

- The rate at which the lender itself borrows money. Determines the floor of the rate the lender can offer.

- Conventional loan

- A loan funded entirely by the lender (no government guarantee), as opposed to an SBA-guaranteed loan.

- Asset-based lending

- A loan secured by specific business assets — receivables, inventory, equipment, or real estate.

- Personal guarantee

- A signed promise by an owner to repay business debt personally if the company cannot.

- Stacking

- Taking on a second or third short-term advance before paying off the first. A common cause of small business financial distress.

Ready to Join the Hive?

Apply now via BeeLine™ and get your funding decision in minutes. Complete in less than 60 seconds.