Business Loans for Small Companies: Types and Benefits

Business loans for small companies fall into eight core types: term loans, lines of credit, working capital loans, SBA loans, equipment financing, merchant cash advances, invoice factoring, and revenue-based financing. The right one depends on speed, cost, use case, and how predictable your revenue is. Most established small businesses qualify for at least three.

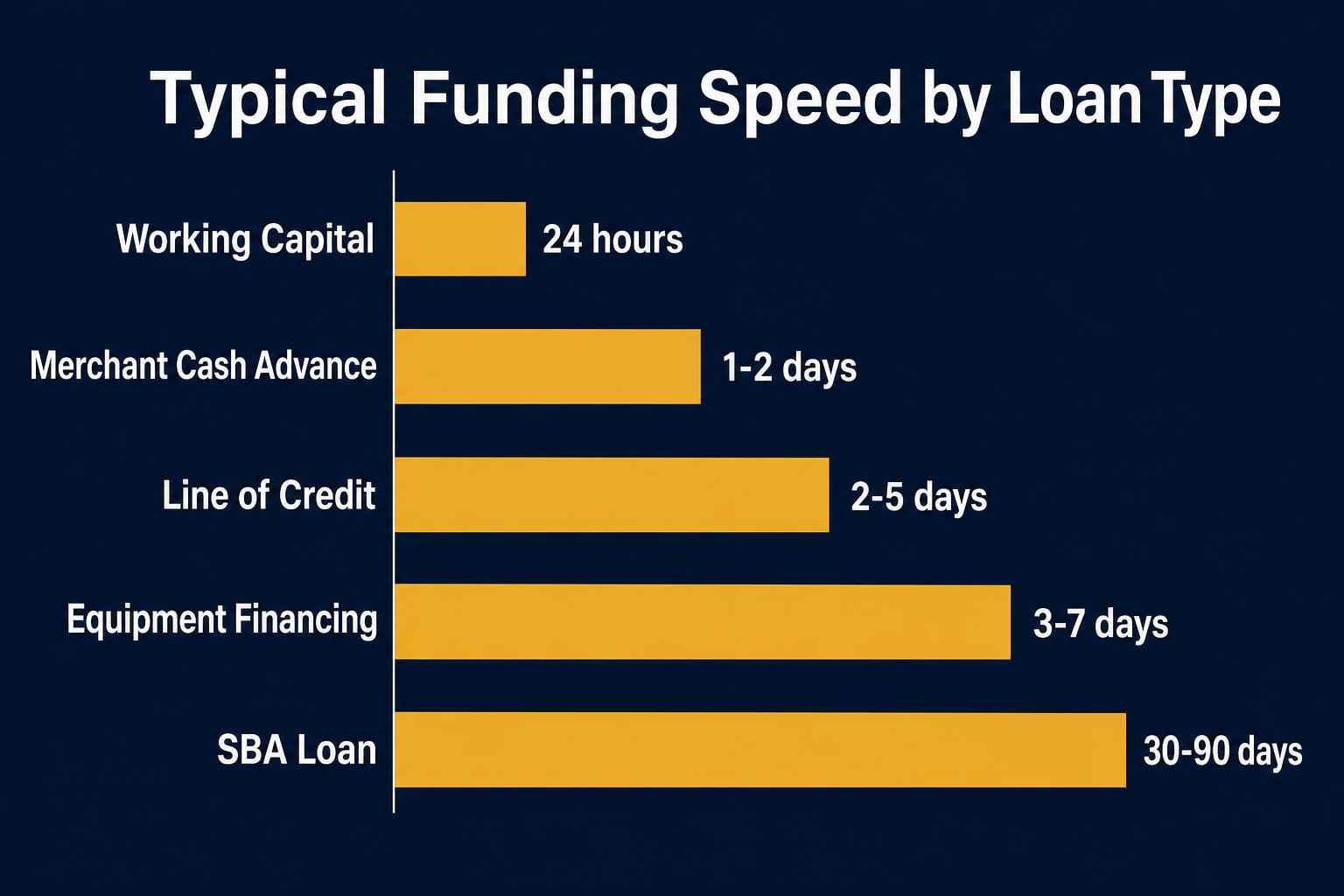

There are eight common types of business loans for small companies in 2026, and each is built for a different problem. Term loans give you a lump sum with fixed payments — best for one-time investments. Lines of credit give you reusable, draw-as-you-need capital — best for cash flow swings. Working capital loans bridge short gaps. SBA loans offer the lowest rates but the longest timelines. Equipment financing uses the asset itself as collateral. Merchant cash advances and revenue-based financing trade higher cost for speed. Invoice factoring unlocks cash tied up in receivables. At BizBee Funding we match small companies with the right product across 100+ vetted lenders, using a soft credit pull, no upfront fees, and funding in as little as 24 hours for qualifying applicants.

Key takeaways

- Eight loan types cover virtually every small-company funding need — the choice depends on use case, not preference.

- Term loans and SBA loans are the lowest-cost options but take 1–6 weeks to fund.

- Lines of credit are the most flexible and reusable, ideal for ongoing cash flow management.

- Working capital loans, MCAs, and revenue-based financing fund in 24–72 hours but cost more.

- Equipment financing typically requires 10%–20% down per NerdWallet — sometimes 0% with strong credit.

- Most U.S. small companies with 6+ months in business and $10K+ monthly revenue qualify for at least three product types.

- Soft-pull prequalification (like BizBee's) lets you compare offers without affecting your credit score.

Who this is for

Owners of established small companies (6+ months in business, $10K+ monthly revenue) who are evaluating funding for the first time and want a plain-English overview before applying.

Operators who already have one loan offer in hand and want to confirm they are looking at the right product type — not just the first product a salesperson pitched.

Newer businesses comparing startup-friendly options like equipment financing, revenue-based financing, or SBA microloans before committing to a higher-cost MCA.

What you need to qualify

Typical small-company requirements across the BizBee Funding partner network. Specific minimums vary by product and lender — some are stricter, others (notably MCAs and revenue-based) are more flexible.

| Requirement | Typical standard |

|---|---|

| Time in business | 6+ months (12+ months unlocks more options) |

| Monthly revenue | $10,000+ in consistent business deposits |

| Personal FICO | 550+ (650+ unlocks lower rates and longer terms) |

| Business bank account | U.S.-based business checking account |

| Bank statements | Most recent 3–6 months |

| Industry | Most for-profit industries; cannabis, adult, and gambling typically excluded |

| Existing debt | Reviewed for stacking limits and payment history |

Best funding options

The eight product categories available through BizBee's lender network. Each links to a dedicated solution page with rates, structure, and applications.

Business Term Loan

Lump-sum loan with fixed monthly payments. Best for one-time investments like expansion, equipment, or acquisitions. $10K–$5M, 1–10 year terms.

Business Line of Credit

Revolving, reusable credit. Draw what you need, pay interest only on the balance. $20K–$500K, ideal for cash flow management.

Working Capital Loan

Short-term funding for payroll, inventory, or seasonal gaps. $5K–$500K, often funded same-day for qualified businesses.

SBA Loan

Government-backed financing with the lowest rates (currently 9.75%–14.75% per NerdWallet, June 2026). Up to $5M per loan. Longer timelines (3–6 weeks).

Equipment Financing

Finance trucks, machinery, kitchen, medical, and shop equipment. The asset serves as collateral, preserving working capital. $10K–$1M.

Merchant Cash Advance

Lump sum repaid via a percentage of future card sales. Fast, flexible, but expensive — factor rates of 1.1–1.5 commonly translate to 60–80% APR per Nav.

Invoice Factoring

Sell outstanding B2B invoices for immediate cash. Typical advance: 80%–95% of invoice value at fees of 1%–5% per 30 days.

Revenue-Based Financing

Capital repaid as a percentage of monthly revenue. Payments flex with sales — useful for seasonal or growth-stage companies.

How Each Loan Type Actually Works for a Small Company

A business term loan is the closest cousin to a personal mortgage: you receive a single lump sum, you sign a fixed amortization schedule, and you make the same payment every month until the balance reaches zero. Terms typically run from 12 to 60 months for short and medium-term loans, and out to 120 months for SBA-style structures. Term loans are the right choice when you know exactly what you need the money for, when that need is a one-time investment (a build-out, an equipment purchase, an acquisition), and when you can absorb a fixed payment regardless of monthly revenue swings.

A business line of credit reverses the structure entirely. Instead of getting all the cash up front, the lender approves a credit limit — say $100,000 — and you draw against it whenever you need to. You pay interest only on the outstanding balance, and as you repay principal the line replenishes. Per Bankrate (Average Business Line of Credit Interest Rates, 2026), APRs range from 3% all the way up to 60%+, with Federal Reserve Q3 2025 averages of 6.99%–7.38% fixed and 7.63%–7.91% variable. Lines are the right tool when your capital need is unpredictable: covering a slow receivable, taking advantage of an inventory discount, or smoothing a seasonal dip.

Working capital loans are short-term lump-sum products designed to bridge a specific gap. Terms typically run 3–18 months, payments are usually daily or weekly via ACH, and approval is fast — often within hours and funded within 24–72. They sit between a term loan (in structure) and an MCA (in speed and cost). For owners who need $25K–$150K to cover a payroll cycle, complete an order, or fund a marketing push, a working capital loan is often the cleanest answer.

SBA loans are partially guaranteed by the U.S. Small Business Administration, which is why their rates are the lowest available — currently 9.75%–14.75% on 7(a) loans per NerdWallet (June 2026), with 504 loans at 5%–7% and microloans at 8%–13%. The trade-off is paperwork and timeline: expect 3–6 weeks from application to funding and a heavier documentation load (tax returns, business plan, debt schedule, projections). The cap on a 7(a) loan is $5 million per loan, and as of July 4, 2026 the SBA raised the cumulative 7(a)+504 limit to $10 million.

Equipment financing is collateralized by the equipment itself, which is why down payments are smaller (typically 10%–20% per NerdWallet, sometimes 0%) and approval is faster than for a comparable unsecured loan. The lender holds a first-position UCC-1 on the asset until the loan is paid off. This is the right structure when the asset is essential to revenue and depreciates predictably — trucks, ovens, CNC machines, diagnostic equipment.

Merchant cash advances, revenue-based financing, invoice factoring, and other alternative products exist for one reason: speed and flexibility for companies that cannot wait three weeks for an SBA decision or cannot pass the credit minimums for a term loan. The honest trade-off is cost. A 1.3 factor rate on a six-month MCA commonly translates to a 60%–80% APR per Nav (Today's Business Loan Interest Rates, Jan 2026). Used surgically for short, high-ROI capital needs, these products work. Used to plug ongoing operating losses, they accelerate financial distress.

Benefits of Borrowing for a Small Company — and the Hidden Costs

The clearest benefit of small business borrowing is the ability to convert future income into present capacity. A $50,000 working capital loan that lets you accept a $200,000 contract you would otherwise have to decline is one of the highest-ROI financial decisions a small company can make. The same is true of a $100,000 equipment loan that doubles your daily output. The benefit is not the loan itself — it is the unit economics that the loan unlocks.

Secondary benefits include cash flow smoothing (you avoid stock-outs, missed payrolls, and emergency vendor decisions), credit building (on-time payments to business lenders build your business credit profile, separate from your personal FICO), and tax positioning (interest on business debt is generally deductible — see your CPA). For owners with strong margins, the after-tax cost of capital can be substantially lower than the headline rate suggests.

The hidden costs are real and worth naming. Daily and weekly ACH debits on short-term loans can shrink the cash buffer that keeps a small company alive in a soft month. Personal guarantees mean a business loan can become a personal liability if the company fails. Stacking — taking on a second or third short-term advance before paying off the first — is the single most common cause of small-company financial distress that we see. And confession-of-judgment clauses (still legal in some jurisdictions) can turn a missed payment into a frozen bank account without warning.

The practical filter is simple: a small-company loan is a good idea when the projected return on the borrowed dollar clearly exceeds the all-in cost of capital and the cash flow can support the repayment in every reasonable scenario, including a 20% revenue dip. If either of those tests fails, borrow less, borrow differently, or wait. A good advisor will tell you the answer is sometimes 'don't borrow right now,' and that honesty is more valuable than a quick approval.

What this typically costs

How the same $100,000 capital need plays out across product types. Rates shown are reasonable mid-market 2026 ranges; your actual offer depends on credit, revenue, time in business, and lender.

| SBA 7(a) — 120 months | ~9.75%–14.75% APR (NerdWallet, June 2026) · ~$1,290–$1,580/mo |

| Bank term loan — 60 months | ~10%–18% APR · ~$2,125–$2,540/mo |

| Online term loan — 36 months | ~14%–35% APR · ~$3,420–$4,160/mo |

| Line of credit (drawn balance) | ~7.6%–60% APR (Fed SBLS Q3'25; Bankrate) · interest-only possible |

| Working capital loan — 12 months | Factor 1.20–1.35 · ~$120K–$135K total payback |

| Merchant cash advance — 6 months | Factor 1.25–1.45 (≈60–80% APR per Nav) · daily/weekly ACH |

How to decide if this is right for you

Use this 5-step framework to narrow your shortlist before you compare specific offers.

-

1

Name the exact use of funds

One-time and quantifiable (equipment, build-out, acquisition) points toward a term loan or SBA. Recurring or unpredictable (cash flow, inventory cycles) points toward a line of credit. Single-asset purchase points toward equipment financing.

-

2

Set your speed requirement

If you need cash this week, SBA is off the table. Working capital, MCA, and revenue-based fund in 24–72 hours. Bank term loans take 2–4 weeks. SBA takes 3–6 weeks.

-

3

Define your maximum payment

Take your trailing 12 months of revenue and stress-test a 20% dip. Whatever monthly debt service you can still cover comfortably is your real ceiling — not whatever a lender approves.

-

4

Match revenue predictability to structure

Predictable monthly revenue tolerates fixed payments well. Highly variable revenue is safer with revenue-based or line-of-credit structures that flex with sales.

-

5

Compare 2–3 offers across product types

Apply through a broker like BizBee with a soft credit pull and compare across product categories — not just within one. The cheapest term loan often beats the fastest MCA even when both are technically 'approved.'

When this makes sense

- When the projected return on the borrowed capital clearly exceeds the all-in cost of the loan.

- When your cash flow can absorb the payment even in a soft month (we model a 20% revenue dip).

- When the use of funds is specific, quantifiable, and time-bound — not a vague 'general working capital' justification.

- When you have at least two comparable offers to evaluate, ideally across different product types.

- When you have a tax and accounting plan for the deductibility of interest and the impact on cash flow.

When to be careful

- When you are borrowing to cover an ongoing operating loss rather than to fund a specific growth investment.

- When you are stacking — adding a second short-term advance before paying off the first.

- When the offer is from a single source you found through a cold call and you have not compared alternatives.

- When the lender will not show you the dollar cost in plain English (factor rate × principal, total payback, daily debit, APR equivalent).

- When the contract includes a confession of judgment or undisclosed brokerage fees.

How this plays out in practice

Real-world example: the contractor who picked the wrong product

Situation: A $1.2M-revenue general contractor needed $80,000 to buy materials for a fixed-price commercial job. He took the first MCA offer at a 1.42 factor rate with daily ACH debits over 8 months. Total payback: $113,600. Effective APR: ~78%. The job's gross margin was 18%, or $216,000 — so the financing cost ate 16% of the margin.

Recommendation: An equipment financing line or a working capital term loan would have priced this around 24%–32% APR for a total cost of roughly $90,000 — saving him over $20,000 on a single job. BizBee placed him on a $250K line of credit two months later, which he now uses revolvingly across multiple projects at ~14% on drawn balances.

Real-world example: the restaurant that did it right

Situation: A 3-unit restaurant group needed $150,000 to open a fourth location. Revenue was $2.4M trailing twelve months, owner FICO 715, 6 years in business.

Recommendation: We placed an SBA 7(a) loan at 11.5% over 10 years. Monthly payment ~$2,110. Total interest cost ~$103,000. The same $150,000 via a 12-month online working capital loan would have cost $35,000–$45,000 in fees — over 4 years, $140,000–$180,000 of compounding cost. The SBA timeline cost them four extra weeks; the wait saved them six figures.

Real-world example: the seasonal landscaper who used a line

Situation: A $600K-revenue landscaper had cash flow that spiked April–October and went near-zero December–February. Crew payroll continued year-round.

Recommendation: A $75,000 line of credit at 14% on drawn balances replaced his prior pattern of stacking two MCAs every winter. Average drawn balance: ~$28,000 for 4 months. Annual interest cost: ~$1,300 vs. ~$22,000 per year previously. Same operational outcome, 94% lower cost.

Not sure which loan type fits your company?

Apply once with a soft credit pull and we'll match you with offers across multiple product types — so you can compare a term loan, a line of credit, and a working capital offer side by side before deciding.

Frequently asked

Common questions

Key facts in one line

- There are eight common types of business loans for small companies in 2026, each built for a different problem.

- Business line of credit APRs range from 3% to 60%+ per Bankrate, with Federal Reserve Q3 2025 averages of 7%–8%.

- SBA 7(a) rates currently run 9.75%–14.75% per NerdWallet (June 2026), with a $5 million cap per loan.

- Equipment financing down payments typically run 10%–20% per NerdWallet, sometimes 0% with strong credit.

- A 1.3 factor rate on a six-month merchant cash advance commonly translates to a 60%–80% APR per Nav.

- Legitimate small business loan brokers never charge upfront fees — they earn referral commissions from the lender at closing.

- Most U.S. small companies with 6+ months in business and $10K+ monthly revenue qualify for at least three product types.

Glossary

Terms worth knowing

- Term loan

- A lump-sum loan repaid in fixed installments over a set period, typically 12–120 months.

- Line of credit

- Revolving access to capital up to an approved limit; you pay interest only on the outstanding balance.

- Working capital loan

- Short-term financing (3–18 months) used to fund payroll, inventory, or operational expenses.

- SBA loan

- A loan partially guaranteed by the U.S. Small Business Administration, typically offering the lowest rates available.

- Equipment financing

- A loan secured by the equipment being purchased; the asset itself serves as collateral.

- Merchant cash advance

- A lump-sum advance repaid via a fixed percentage of future credit card sales. Quoted as a factor rate, not an interest rate.

- Factor rate

- A multiplier (e.g., 1.30) applied to the advance principal to determine total payback. Not equivalent to APR.

- Soft credit pull

- An inquiry that does not affect your FICO score, used for prequalification across multiple lenders.

- Personal guarantee

- A signed promise to repay business debt personally if the business cannot.

Ready to Join the Hive?

Apply now via BeeLine™ and get your funding decision in minutes. Complete in less than 60 seconds.