What Is an Equipment Financing Loan?

A loan used to buy business equipment, secured by the equipment itself. Typically funds 80%–100% of purchase price, 2–7 year terms, rates from 7% APR (strong credit) to 30% APR (subprime). Easier to qualify for than unsecured funding.

Equipment financing is a business loan used specifically to purchase business equipment, vehicles, machinery, kitchen gear, medical devices, technology, where the equipment itself serves as the collateral. Because the loan is collateralized by the asset, approval is often easier and rates are typically lower than unsecured working capital products.

Key takeaways

- The equipment being purchased is the collateral, so approval is easier than for unsecured loans.

- Most lenders finance 80%–100% of the equipment cost, with terms matched to expected useful life (2–7 years).

- Rates typically range from 7% APR (bank, strong credit) to 30% APR (online, subprime).

- Soft costs — delivery, installation, training, taxes, can often be rolled in.

- Equipment financing preserves your working capital and credit lines for operations.

Who this is for

Businesses buying a specific piece of equipment costing $5,000 or more.

Owners who want to spread the asset's cost over its useful life and keep cash reserves intact.

What you need to qualify

| Requirement | Typical standard |

|---|---|

| Time in business | 6+ months (12+ for best rates) |

| Monthly revenue | $10,000+ |

| Personal credit | 550+ FICO (650+ for low rates) |

| Down payment | 0%–20% depending on credit and equipment age |

| Equipment | New or used; titled or non-titled |

Why equipment financing is the easiest business loan to qualify for

Equipment financing is structurally different from every other business loan because the equipment itself is the collateral. If the borrower defaults, the lender can repossess and resell the equipment, recovering most of the principal. That collateral coverage means lenders accept weaker credit, shorter time in business, and lighter financial documentation than they would on any unsecured product.

BizBee equipment partners regularly approve borrowers with 550 FICO and 6 months in business, a profile that would be declined on an unsecured working capital loan. Down payment requirements scale with credit: strong-credit borrowers buying titled equipment often get 100% financing; subprime borrowers buying specialty equipment may need 10–20% down.

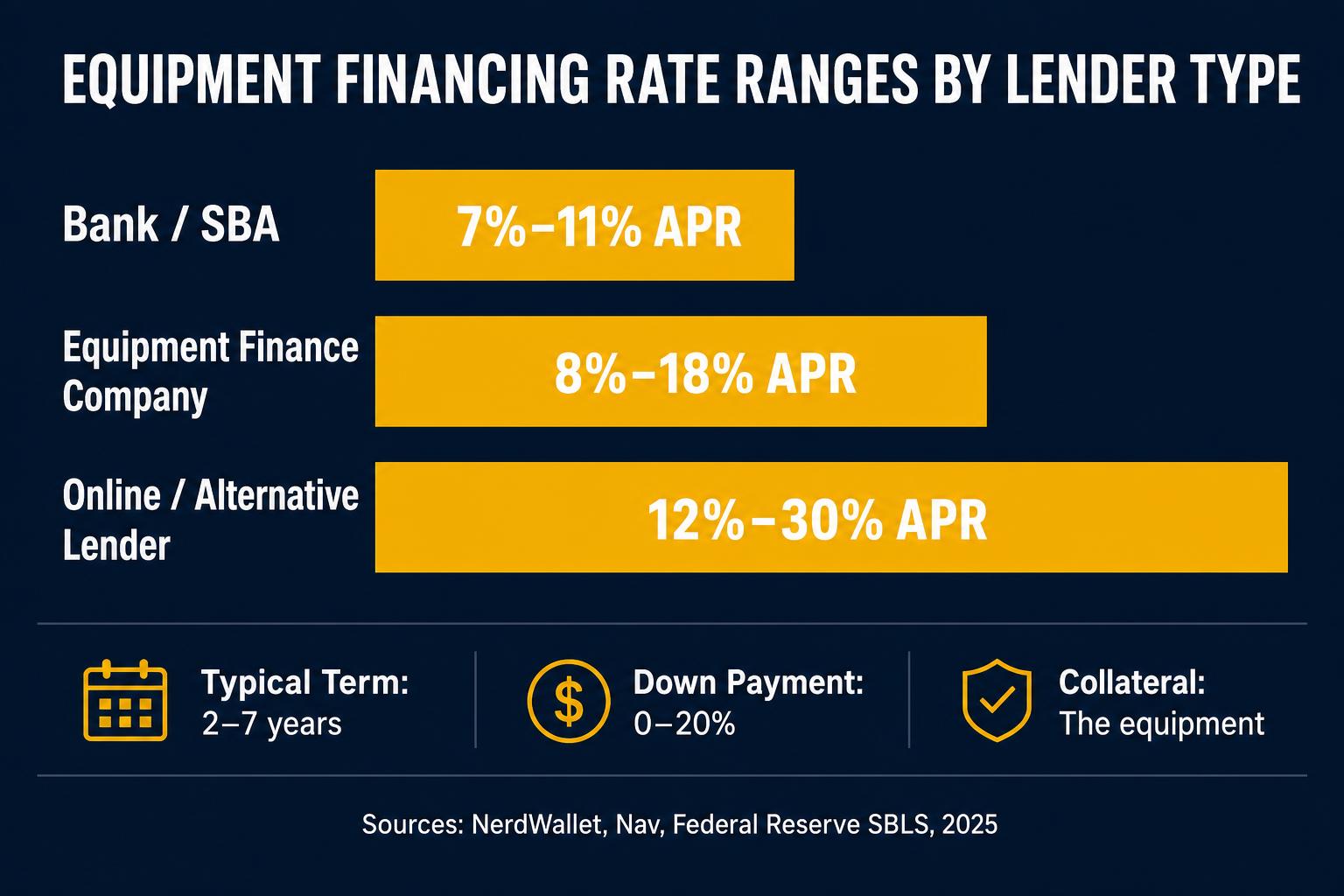

Equipment financing rates and term structure

Per NerdWallet's 2026 equipment financing data, bank-issued equipment loans run 7%–12% APR for strong-credit borrowers, online equipment loans run 12%–22% APR for mid-credit borrowers, and online subprime equipment loans run 22%–30% APR. Terms are matched to the equipment's expected useful life, typically 24–84 months.

NerdWallet's 2026 small-business down payment data shows that equipment financing down payments typically run 10%–20%, sometimes up to 30% for subprime credit or specialty equipment. Most prime borrowers buying standard titled equipment qualify for 0% down.

Equipment financing vs equipment leasing

Financing means the borrower owns the equipment from day one and pays it off over the term. Leasing means the borrower rents the equipment over the term, with an option (or obligation) to buy at end-of-term. Leases usually price slightly cheaper than financing but lack the asset-build benefit.

Choose financing for equipment with a long useful life (heavy machinery, vehicles, kitchen equipment) where ownership matters. Choose leasing for fast-depreciating equipment (technology, software) where return rights matter more than ownership.

Section 179 and bonus depreciation, the 2026 tax math

Section 179 of the Internal Revenue Code lets businesses deduct the full purchase price of qualifying equipment in the year it's placed in service, up to the 2026 limit of $1,250,000 with a phase-out starting at $3,130,000 in total equipment purchases (IRS Rev. Proc. 2025-32). Bonus depreciation is set at 40% for equipment placed in service in 2025 and 20% in 2026 under the current TCJA phase-down schedule, with Section 179 fully deductible above bonus where it applies. Financed equipment qualifies the same as cash-purchased equipment, which is why equipment financing is uniquely tax-efficient, the borrower deducts the full purchase price in year one while paying for it over 2–7 years.

Worked example: a $200K piece of equipment financed at 12% APR over 60 months. Year-one Section 179 deduction = $200K. At a 24% effective business tax rate, that's $48K of immediate tax savings on cash that hasn't yet left the business. Net first-year economics: roughly $44K in payments made, $48K in tax savings, $4K net cash positive in year one before the equipment even generates revenue.

Limits and caveats worth confirming with a CPA before signing: Section 179 deduction cannot exceed the business's taxable income (excess carries forward), some used equipment is excluded, the equipment must be placed in service (not just ordered or paid for) before December 31 to qualify in that tax year, and state-level Section 179 conformity varies — California in particular caps Section 179 at $25,000 against state tax. The federal benefit is consistent nationwide; state-level treatment is not.

What underwriters score on an equipment financing application

Equipment underwriting is the most asset-driven scoring in commercial lending. The four primary inputs are: equipment type and age (titled equipment like trucks and trailers finance easier than non-titled like specialty manufacturing tools; new equipment finances easier than 10+ year used), purchase price relative to wholesale value (lenders typically advance 80%–100% of fair market value, never above), borrower credit and revenue (personal FICO and 3–6 months of bank statements), and supplier or vendor relationship (deals with established equipment dealers move faster than private-party transactions).

Specific equipment categories with the easiest approval paths in 2026: medium and heavy-duty trucks, trailers, construction equipment under 10 years old, restaurant equipment from major manufacturers, dental and medical equipment with strong resale markets, and standard machine-shop tooling. Categories that face more scrutiny: solar installations, cannabis-industry equipment, restaurant equipment from defunct manufacturers, software-only purchases, and any equipment financed for less than 50% of dealer invoice value.

Practical application sequence: get a written quote from the equipment vendor (must include make, model, year, serial number, total price including soft costs), apply through BizBee with the quote attached, soft-pull pre-qualification returns rate ranges within hours, vendor invoice and signed financing agreement get exchanged in 1–3 business days, funds wire directly to the vendor at closing. The borrower never handles cash, the equipment ships once the wire is confirmed.

What this typically costs

Typical 2025–2026 equipment financing ranges. Sources: NerdWallet 2025, Nav, Federal Reserve SBLS.

| Bank equipment loan (strong credit) | 7.00% – 12.00% APR |

| Online equipment loan (mid credit) | 12.00% – 22.00% APR |

| Online equipment loan (subprime) | 22.00% – 30.00% APR |

| Typical term | 24–84 months, matched to useful life |

| Down payment | 0%–20% (often 0% for titled equipment) |

How to decide if this is right for you

Five gates before signing equipment financing.

-

1

Will the equipment produce revenue exceeding monthly payment?

Incremental revenue or savings should comfortably exceed the monthly payment. If not, leasing or deferring is usually better.

-

2

Match term length to useful life

Don't finance 7-year machinery over 36 months (cash-flow strain) or 3-year equipment over 84 months (paying for assets you'll no longer use).

-

3

Decide finance vs. lease

Long useful life + ownership matters → finance. Obsolescence risk + return rights matter → lease.

-

4

Compare titled vs. non-titled financing terms

Titled equipment (vehicles, trailers) usually finances at lower rates and longer terms than non-titled (kitchen gear, IT).

-

5

Get supplier invoice + spec sheet ready

Equipment lenders fund against the invoice, not against a generic estimate. A signed invoice accelerates closing.

When this makes sense

- The equipment will produce revenue or savings greater than its monthly payment.

- You want to preserve cash and other credit lines for operations.

- You expect to use the equipment for 3+ years.

When to be careful

- Equipment becomes obsolete fast (some tech), leasing may beat financing.

- If you may not use the equipment full-time, a lease with return rights protects the downside.

How this plays out in practice

Contractor buying a $90K skid steer

Situation: Construction business, 650 FICO, 3 years in business; buying a new titled skid steer.

Recommendation: 60-month equipment loan at 10–13% APR with 0% down; titled equipment + strong credit typically qualifies for 100% financing.

Restaurant replacing aging kitchen line

Situation: Restaurant needs $120K in commercial kitchen equipment; 620 FICO, 18 months in business.

Recommendation: 48-month equipment loan at 15–20% APR with 10–15% down; non-titled equipment + mid credit typically requires some down payment.

Tech startup considering server hardware

Situation: Software company needs $80K in server hardware expected to be obsolete within 36 months.

Recommendation: Lease, not finance. Fast-depreciating equipment with obsolescence risk is structurally better as a lease with return rights.

Get an equipment financing quote

Fast soft-pull pre-qualification across BizBee equipment lenders.

Frequently asked

Common questions

Glossary

Terms worth knowing

- Titled equipment

- Equipment with a state-issued title (vehicles, trailers, some heavy machinery). Usually qualifies for cheaper financing and longer terms than non-titled.

- Useful life

- The number of years the equipment is expected to be productive. Lenders match financing term to useful life when possible.

- Section 179

- An IRS provision that lets businesses deduct the full purchase price of qualifying equipment in the year of purchase rather than depreciating it over years.

- Equipment lease

- A rental agreement for equipment over a fixed term, often with end-of-term purchase or return options. Distinct from equipment financing.

Ready to Join the Hive?

Apply now via BeeLine™ and get your funding decision in minutes. Complete in less than 60 seconds.