What Is Purchase Order Financing?

Lender pays your supplier so you can fulfill a large confirmed customer order, then is repaid (plus a 2%–6% per-30-day fee) when your customer pays the resulting invoice. Best for product resellers, wholesalers, and importers with confirmed POs they can't self-fund.

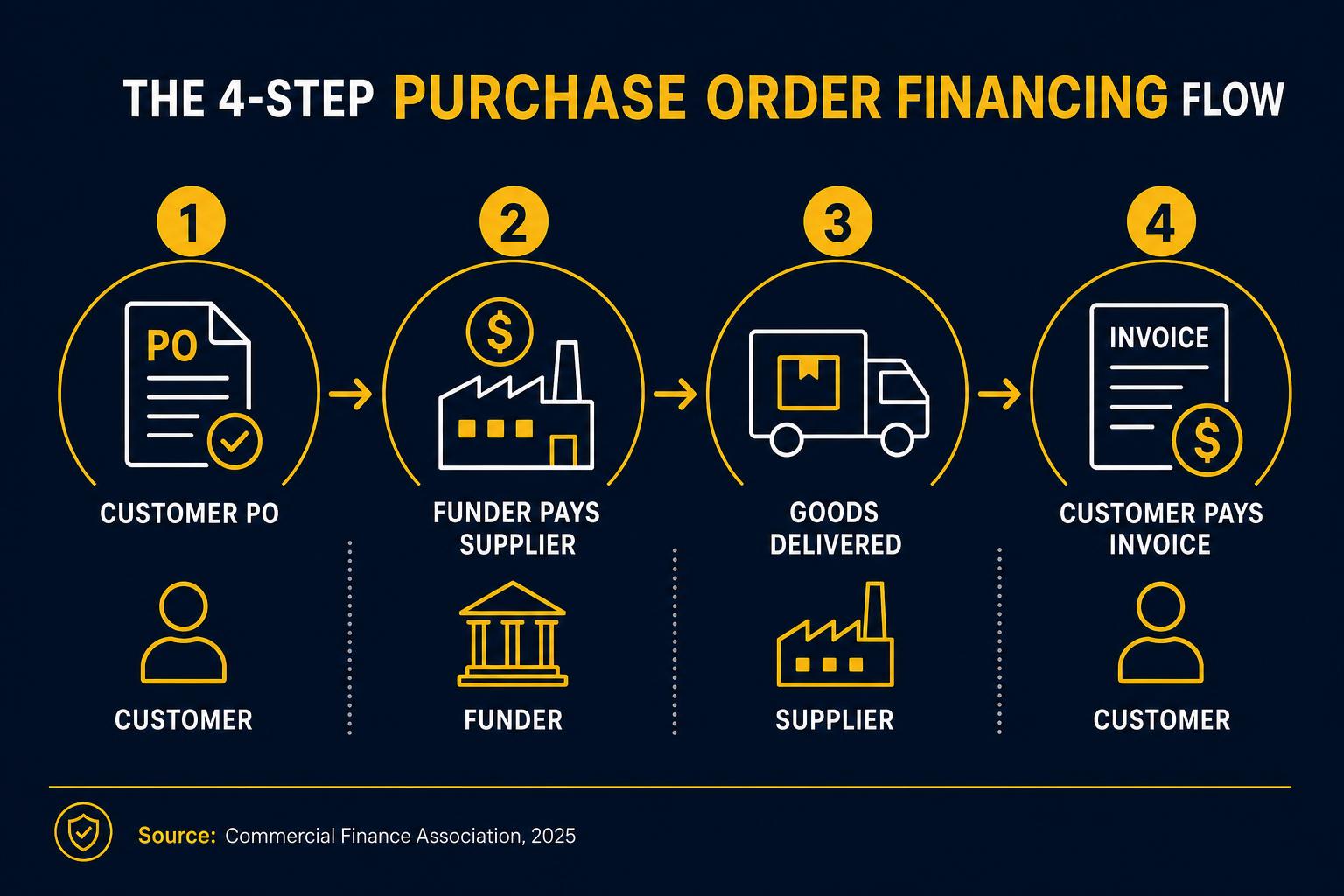

Purchase order (PO) financing is a short-term funding arrangement where a lender pays your supplier directly so you can fulfill a confirmed customer purchase order you couldn't otherwise afford to produce. After your customer pays the invoice, the PO funder is repaid in full plus a fee, and the remainder is released to your business.

Key takeaways

- PO financing covers supplier costs, not operating expenses, it's order-specific.

- Funds the supplier directly; the borrower never sees the cash.

- Repaid when the end customer pays the resulting invoice (often via factoring of that invoice).

- Fees typically 2%–6% per 30-day period; effective APR can run 25%–80% depending on cycle length.

- Approval depends mostly on your customer's credit and the supplier's ability to deliver.

Who this is for

Product resellers, wholesalers, distributors, and importers with confirmed customer POs they can't self-fund.

Newer businesses landing their first large order from a creditworthy buyer.

What you need to qualify

| Requirement | Typical standard |

|---|---|

| Customer | Creditworthy commercial or government buyer |

| Product margin | 20%+ gross margin (lender needs spread) |

| PO type | Confirmed, non-cancellable customer PO |

| Supplier | Reputable, able to deliver to spec |

| Industry | Resale of finished goods (not services or custom builds) |

How purchase order financing actually works

Purchase order (PO) financing is a specialized short-term funding structure designed for one specific situation: a small business has landed a confirmed customer purchase order larger than it can self-fund. The PO funder pays the borrower's supplier directly (often via letter of credit) so the goods can be produced and shipped. When the customer pays the resulting invoice, the PO funder is repaid the supplier cost plus a fee.

Crucially, the borrower never sees the cash. The funder pays the supplier; the customer pays the funder; the borrower gets the margin. This structure makes PO financing inherently safer for the funder and inherently more expensive for the borrower (fees typically 2–6% per 30-day period, with effective APRs of 25–80%+ per NerdWallet 2026 and Kapitus industry data).

Why PO financing has higher fees than invoice factoring

Invoice factoring buys a delivered, invoiced receivable, the risk is collection timing. PO financing funds production of goods that haven't yet been delivered — the risk is production failure, shipping delay, or customer dispute. Higher risk justifies the higher fee.

Per NerdWallet 2026 and Kapitus benchmarks, PO funders typically advance up to 100% of supplier cost at fees of 2–6% per 30 days. Many borrowers pair PO financing on the front end with invoice factoring on the back end to compress the total funding cycle.

Who PO financing actually works for

PO financing fits product resellers, wholesalers, importers, and distributors landing large orders from creditworthy commercial or government customers. It requires 20%+ gross margin, finished goods (not custom builds or services), and a supplier with a track record of on-time delivery to spec.

PO financing does not work for service businesses, custom-build manufacturers, thin-margin commodity resellers, or businesses with uncreditworthy customers.

The full PO financing lifecycle, step by step

Step 1, application and customer approval (1–2 weeks for first deal). Borrower submits the signed customer PO, supplier quote, and basic business documents. The PO funder runs commercial credit on the customer (D&B, Experian Business, public-record review) and validates the supplier's ability to deliver. Subsequent transactions with the same customer-supplier pair often close in 2–4 days.

Step 2, supplier payment and production (timing varies by industry). Funder pays supplier directly via wire, ACH, or in the case of overseas suppliers, an irrevocable letter of credit. Supplier begins production; borrower coordinates logistics and ensures product specs match the customer PO exactly. Any dispute at this stage delays repayment and accrues additional PO fees.

Step 3, delivery, customer acceptance, and invoicing (1–4 weeks depending on shipping). Goods ship to customer, customer accepts delivery, borrower issues invoice. Many PO deals convert here into invoice factoring of that specific invoice, accelerating final repayment to the PO funder. Step 4, customer payment and PO funder repayment (30–90 days after invoicing). When the customer pays the invoice, the PO funder is repaid the supplier cost plus accrued fees, and the borrower receives the remaining margin. Total cycle from PO acceptance to borrower payout typically runs 45–120 days.

PO financing vs supplier trade credit vs inventory financing

Supplier trade credit (net-30, net-60 terms from the supplier directly) is always the cheapest option when available — there's no PO funder fee, only an opportunity-cost of working capital. Most established suppliers extend trade credit to borrowers with documented payment history, but new buyer relationships and oversized orders frequently exceed what the supplier is willing to extend on open account. PO financing fills that gap.

Inventory financing differs structurally, it funds general inventory holding rather than a specific customer order. An importer stocking a warehouse for the next two quarters uses inventory financing or a LOC. The same importer who suddenly lands a $500K confirmed order beyond standard stocking levels uses PO financing for the incremental production. Many product businesses run both products in parallel: inventory financing for baseline operations, PO financing for breakout orders.

Pure cost comparison on a 60-day cycle: trade credit ≈ 0% direct fee (opportunity cost only), inventory financing ≈ 2.5%–5% (annualized 15%–30% APR), PO financing ≈ 4%–8% on the supplier-cost portion (annualized 25%–80%). The order in which to exhaust options is consistent: maximize trade credit first, deploy inventory financing or LOC for standard volume, reserve PO financing for confirmed orders that exceed both. BizBee advisors structure the full capital stack to minimize total cost across the order cycle.

PO financing in cross-border and overseas-supplier scenarios

PO financing becomes meaningfully more complex when the supplier is overseas. The funder typically issues an irrevocable letter of credit (LC) to the foreign supplier, often confirmed by a correspondent bank in the supplier's country. LC fees (0.5–2.5% of LC face value per quarter per SBA Office of International Trade 2025 guidance) stack on top of the per-30-day PO fee, and FX exposure has to be allocated explicitly, either the borrower or the funder takes the FX risk, never both.

Lead times shift dramatically. A US-to-US PO cycle might run 45–60 days; an Asia-to-US PO cycle frequently runs 90–150 days once ocean freight, customs clearance, and last-mile US delivery are included. Every additional 30 days adds another full PO-fee increment, so a 5% per-30-day fee on a 120-day cycle is roughly 20% of supplier cost, gross margin must be sized accordingly.

Common cross-border PO structures pair the LC on the front end with invoice factoring on the back end the moment goods clear US customs. This compresses borrower cash-out by 30–60 days and significantly improves blended cost. BizBee advisors model the full LC + freight + factoring stack before signing the PO so margin reality is visible before commitment, not after the goods are in transit.

What this typically costs

Illustrative PO financing economics. Sources: NerdWallet 2025, Commercial Finance Association data.

| Customer PO value | $500,000 |

| Supplier cost | $350,000 (paid by PO funder) |

| PO fee | 3% per 30 days |

| Cycle (production + payment) | 60 days |

| Total PO fee | ~6% × $350K = $21,000 |

| Gross margin after fee | $129,000 (≈ 26%) |

How to decide if this is right for you

Five gates before pursuing PO financing.

-

1

Is the purchase order confirmed and non-cancellable?

PO funders require a signed, non-cancellable PO. Verbal commitments or LOIs don't qualify.

-

2

Is your gross margin 20%+ after PO fees?

Model fee + cycle time. If margin after fees is under 15%, the deal is too risky for both sides.

-

3

Is the customer's commercial credit strong?

PO funders underwrite the customer's ability to pay. Large corporates and government buyers fund easily.

-

4

Can your supplier deliver on spec, on time?

Production failure is the single biggest cause of PO financing losses. Choose suppliers with track records.

-

5

Plan the back-end factoring

Most PO deals work best paired with invoice factoring of the resulting invoice, accelerates customer payment.

When this makes sense

- You have a confirmed PO larger than you can self-fund.

- Your gross margin is at least 20% (lender fee needs room).

- The product is finished goods, not custom-built services.

When to be careful

- Thin-margin products may not survive PO fee structure.

- Customer disputes after delivery delay repayment and accrue fees.

- Service businesses generally cannot use PO financing.

How this plays out in practice

Wholesaler with first major retail PO

Situation: Wholesale business lands a $400K PO from a national retailer; supplier cost is $280K; borrower can't self-fund.

Recommendation: PO financing fits. Funder pays supplier; goods ship; retailer pays in 60 days. Pair with invoice factoring of the back-end invoice.

Importer with confirmed customer order

Situation: Importer needs to pay overseas supplier $150K to fulfill $250K confirmed US customer order; 90-day cycle.

Recommendation: PO financing via letter of credit to overseas supplier; back-end invoice factored when goods land.

Service business with large consulting contract

Situation: Consulting firm lands $300K service contract requiring upfront staffing.

Recommendation: Not a fit (no finished goods, no supplier). Use working capital or invoice factoring instead.

Government contractor with multi-tranche PO

Situation: Federal contractor wins a $1.2M PO with quarterly delivery tranches; supplier requires 60% deposit per tranche.

Recommendation: PO financing fits per tranche; structure as a revolving PO facility against the master contract; pair with government-receivables factoring at delivery for fastest repayment.

Got a big PO you can't fulfill alone?

BizBee will quickly assess PO funding fit and price the order.

Frequently asked

Common questions

Glossary

Terms worth knowing

- Purchase order (PO)

- A signed, non-cancellable order from a customer to buy specified goods at agreed terms. The collateral PO financing is built around.

- Letter of credit

- A bank-issued instrument guaranteeing supplier payment on fulfillment of specified conditions. Often used to fund overseas suppliers in PO financing.

- Trade credit

- Supplier financing in which the supplier accepts payment after delivery (e.g., net-30). An alternative to PO financing when the supplier extends credit.

- Fulfillment cycle

- The time from supplier payment through delivery to customer payment. PO financing fees accrue per 30 days of this cycle.

- Confirmed letter of credit

- An LC where a second bank (typically in the supplier's country) guarantees payment if the issuing bank fails, reducing supplier risk on overseas PO financing transactions.

- Advance rate

- The percentage of supplier cost a PO funder will pay upfront. Typically 100% of supplier cost in PO financing, vs 70–90% in invoice factoring.

Ready to Join the Hive?

Apply now via BeeLine™ and get your funding decision in minutes. Complete in less than 60 seconds.