What Is Revenue-Based Financing?

A lump sum repaid as a fixed % of monthly revenue (usually 3%–10%) until you've paid back 1.2x–1.6x of the original amount. Payments flex with revenue, total cap is fixed. Better fit for growth-stage businesses than MCAs.

Revenue-based financing (RBF) is a funding product where a business receives a lump sum and repays it through a fixed percentage of monthly revenue until a pre-agreed multiple (typically 1.2x–1.6x of the funded amount) is paid back. Payments flex with revenue, high in strong months, lower in slow months, but the total payback amount is capped at the multiple.

Key takeaways

- RBF payments scale with revenue: high months = higher payment, low months = lower.

- Total payback is capped at a multiple (typically 1.2x–1.6x), not open-ended.

- Term length is variable, depends on how fast revenue scales.

- Common in SaaS, e-commerce, and subscription businesses with predictable recurring revenue.

- Different from MCAs: RBF repayment % is of monthly revenue, not daily ACH; usually no UCC, no PG required.

Who this is for

E-commerce, SaaS, subscription, or DTC brands with $20K+ monthly revenue and a clear path to growth.

Founders who want to avoid daily ACH pressure of MCAs and don't want to give up equity.

What you need to qualify

| Requirement | Typical standard |

|---|---|

| Time in business | 6–12 months typical |

| Monthly revenue | $20,000+ recurring |

| Revenue type | Stable, recurring, or subscription |

| Channels accepted | Stripe, Shopify, PayPal, ACH, etc. |

| Personal credit | Often not required (varies) |

How revenue-based financing actually works

Revenue-based financing (RBF) delivers a lump sum upfront in exchange for a fixed percentage of the borrower's monthly revenue until a pre-agreed multiple (typically 1.2x–1.6x of the funded amount) is repaid. Unlike an MCA, where the daily ACH is a fixed dollar amount that doesn't flex with revenue, RBF payments scale: when revenue is strong, payments are higher and payoff accelerates; when revenue is weak, payments shrink proportionally and term extends.

RBF is most commonly funded by specialty platforms (Capchase, Pipe, Clearco, Lighter Capital) that integrate directly with revenue data sources — Stripe, Shopify, banking APIs, to underwrite in near-real-time. Funding decisions are often automated and completed within 24–72 hours.

Why RBF beats MCAs for the right businesses

For SaaS, subscription, and e-commerce businesses with predictable recurring revenue, RBF is structurally superior to an MCA. Payments flex with revenue (no daily-debit pressure during slow weeks), most RBF products require no personal guarantee or UCC filing, and the total payback is capped at a multiple rather than open-ended.

RBF is not always cheaper than an MCA on a strict cost basis, a 1.35x multiple on a fast-growing SaaS business can convert to a high effective APR if revenue scales quickly. The structural benefits usually justify the cost for businesses that qualify.

When RBF is the wrong product

RBF is wrong for one-time project funding with no revenue link, for businesses with declining revenue, and for businesses considering equity instead. It's also a poor fit for businesses with lumpy, non-recurring revenue.

Pure project-based revenue (construction, agency work) typically doesn't underwrite well for RBF. These businesses are better served by traditional working capital or invoice factoring.

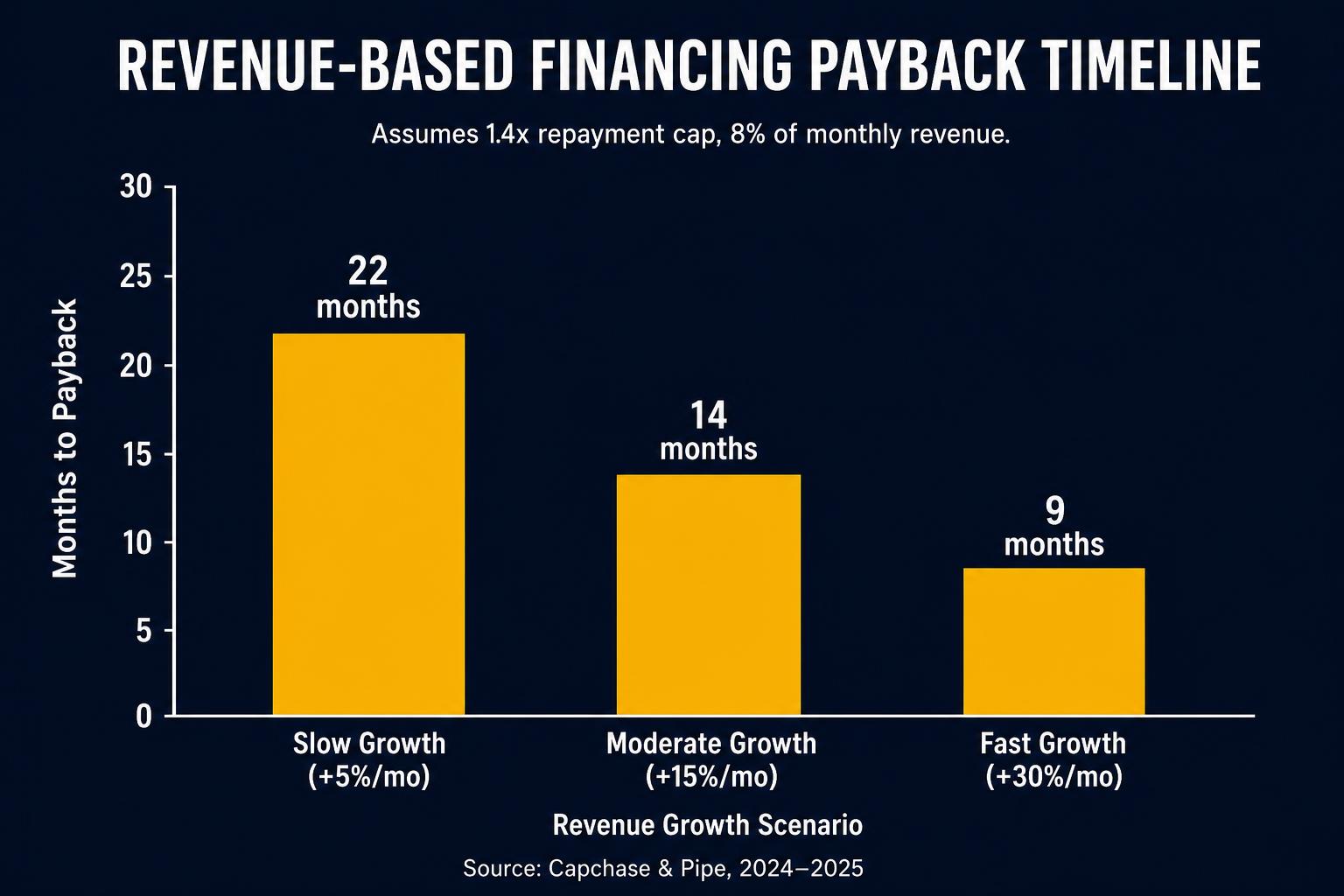

How RBF's effective cost scales with growth, the math owners miss

RBF total payback is capped at the multiple (typically 1.2x–1.6x), but the effective APR is not capped, it moves with revenue growth. A $100K advance at a 1.35x multiple ($135K total payback) and a 6% revenue share repaid over 45 months at $50K/mo revenue carries an effective APR of roughly 18%. The same deal repaid in 15 months at $150K/mo revenue carries an effective APR closer to 50%. Faster growth means a faster payoff, which means a higher annualized cost on the locked $35K spread.

This is the inverse of intuition. Most founders assume faster growth makes the financing 'cheaper' because it's paid back sooner — but the total dollars repaid are fixed at the cap, so faster repayment compresses the same cost into less time. Three practical implications: (1) RBF tends to look most attractive for businesses that expect steady, predictable growth rather than explosive growth; (2) RBF terms with optional early-payoff discounts can dramatically improve outcomes for fast-growers; (3) for true breakout-growth businesses, equity often wins over RBF on a pure cost basis once expected effective APR climbs above ~40%.

Modeling discipline matters more on RBF than any other commercial product. Before signing, build three revenue scenarios (base, upside, downside) and compute the effective APR in each. If the upside scenario produces an effective APR above 50%, renegotiate the multiple down or look at a term loan alternative. BizBee advisors run this three-scenario model on every RBF offer before recommending acceptance.

RBF vs MCA vs term loan, the side-by-side decision

Same $100K need, three structures, 12-month horizon. RBF at 1.35x multiple, 6% revenue share, $80K/mo average revenue = roughly $4,800/mo payment, ~28-month payoff, ~24% effective APR. MCA at factor 1.30, $250/day debit, $40K/mo paid = ~10-month payoff, ~55% effective APR. Term loan at 22% APR, 36-month amortization = ~$3,800/mo payment, fixed total interest ~$36K.

On effective APR alone, the term loan wins. On cash-flow flexibility (payment scales with revenue), RBF wins. On speed and credit accessibility, the MCA wins. On structural protection (no PG, no UCC on most RBF products), RBF wins. The right choice depends on which axis matters most for the borrower's specific risk profile.

Common pattern at BizBee: RBF for recurring-revenue businesses that prioritize cash-flow flexibility and are comfortable with 20%–30% effective APR; term loan for businesses with strong credit and a discrete, fully-deployed use of funds; MCA only when speed or credit tier rules out the other two products. Stacking is never recommended, pick the product that fits the use, then refinance into cheaper capital after building 6–12 months of clean payment history.

What this typically costs

Illustrative RBF cost. Sources: Pipe, Capchase, Clearco published 2024–2025 ranges.

| Funded amount | $100,000 |

| Multiple (cap) | 1.35x |

| Total payback | $135,000 |

| Revenue share | 6% of monthly revenue |

| Implied term @ $50K/mo revenue | ~45 months |

| Implied term @ $150K/mo revenue | ~15 months |

How to decide if this is right for you

Five gates to decide whether RBF fits your business.

-

1

Is your revenue recurring or subscription?

SaaS, subscription e-commerce, DTC with high repeat purchase = strong fit. Project-based or lumpy revenue = poor fit.

-

2

Is monthly revenue $20K+ and growing?

Most RBF platforms set $20K/month as the floor; growth trajectory matters more than absolute size.

-

3

Compare the implied APR against an MCA and a term loan

RBF multiple converts to effective APR based on growth rate. Model all three at your projected revenue.

-

4

Confirm you can integrate revenue data

Most RBF platforms require API access to Stripe, Shopify, or banking. Manual underwriting is rare.

-

5

Decide whether you'd otherwise raise equity

If the alternative is equity dilution, RBF is almost always preferred. If the alternative is a term loan and you qualify, term loan is usually cheaper.

When this makes sense

- Your revenue is recurring or seasonal and you want payments that flex.

- You're growth-stage and don't want to give up equity.

- You don't qualify for bank/SBA but want better terms than an MCA.

When to be careful

- If revenue rockets, you pay back faster, and your effective rate rises.

- Not ideal for one-time project funding with no revenue link.

How this plays out in practice

SaaS company with $60K MRR funding growth

Situation: B2B SaaS with $60K MRR growing 8%/month; needs $300K to scale paid marketing.

Recommendation: RBF is ideal. Recurring revenue, strong growth, alternative would be equity dilution. Expect 1.3x–1.4x multiple at 6–10% of monthly revenue.

E-commerce DTC brand funding inventory

Situation: Shopify-only DTC brand, $80K/month revenue, 25% gross margin; needs $150K for Q4 inventory.

Recommendation: RBF appropriate; integrates with Shopify cleanly. Compare against inventory financing, pick whichever has lower implied cost.

Agency with lumpy project revenue

Situation: Marketing agency, $50K/month revenue but lumpy by quarter; needs $80K for hiring.

Recommendation: RBF is a poor fit. Use a LOC or working capital term loan instead.

DTC brand evaluating RBF vs equity raise

Situation: Consumer DTC brand, $120K MRR growing 12%/month, considering a $1M Series A vs $750K RBF facility for inventory and ad spend.

Recommendation: Run both pro formas to 36 months. RBF at 1.4x on $750K = $1.05M total payback; effective APR likely 25%–35% given growth rate. Series A at $5M post-money on $1M check = 20% dilution forever. RBF wins if the founder values control and the growth math says next round will be priced at $20M+. Equity wins if the next 18 months are make-or-break and downside cash protection matters more than ownership.

Get an RBF quote in 24 hours

Connect your Stripe/Shopify and BizBee partners price your offer fast.

Frequently asked

Common questions

Glossary

Terms worth knowing

- Multiple (RBF)

- The total payback cap on an RBF deal, expressed as a multiplier on the funded amount (e.g., 1.35x = $135K total payback on a $100K funded amount).

- Revenue share

- The percentage of monthly revenue remitted to the RBF funder until the multiple is paid back. Typically 3–10%.

- Recurring revenue

- Subscription, SaaS, or contract-based revenue that recurs predictably each month. The primary RBF underwriting input.

- Dilutive

- Reducing existing owners' ownership percentage by issuing new equity. RBF is non-dilutive; venture capital is dilutive.

- Remittance adjustment

- The contractual mechanism that scales an RBF payment up or down with monthly revenue. The specific revenue-measurement window (trailing 30 days vs prior calendar month) and adjustment frequency vary by funder.

- Implied APR

- The effective annualized cost of an RBF deal, calculated from the multiple, revenue share, and projected revenue. Not displayed on most RBF term sheets; borrowers must compute it to compare against term loans.

Ready to Join the Hive?

Apply now via BeeLine™ and get your funding decision in minutes. Complete in less than 60 seconds.